CoreWeave ($CRWV) IPO S-1: Everything You Need to Know

As AI takes center stage, attention is shifting to the companies driving its growth. CoreWeave, a specialized cloud provider for GPU-intensive computing, has filed for an IPO, unveiling its S-1 filing. The company highlights its rapid expansion and strong position in the AI infrastructure market. It plans to list its shares on Nasdaq under the ticker symbol $CRWV. The filing details CoreWeave’s growth trajectory, business model, key financial figures, and the risks and opportunities ahead. Here’s everything we learned from the company’s filing.

Company History

CoreWeave was founded in 2017 as a cryptocurrency mining venture called Atlantic Crypto by Michael Intrator, Brian Venturo, and Brannin McBee. Originally commodities traders, the founders used GPU rigs to mine Ethereum. After the 2018 crypto crash, they pivoted in 2019, rebranding as CoreWeave and repurposing their extensive GPU inventory for cloud computing services.

Initially, CoreWeave provided on-demand GPU power for tasks such as visual effects rendering and other compute-intensive workloads. The company fully exited crypto mining in 2022 when Ethereum transitioned to proof-of-stake. While Ethereum mining still accounted for 61% of its $15.8 million revenue in 2022, it was discontinued afterward.

Since then, company has focused exclusively on cloud-based GPU infrastructure for enterprises, particularly in artificial intelligence (AI) and machine learning applications. This strategic shift positioned the company to capitalize on the soaring demand for AI computing in the years that followed.

Business Model & Revenue Streams

CoreWeave is a cloud infrastructure provider specializing in GPU-based computing, branding itself as an “AI hyperscaler.” It operates large data centers filled with graphics processing units (GPUs) and rents out computing power to customers on a cloud basis. Clients use company’s servers for demanding workloads such as AI model training and inference, graphics rendering, and other high-performance computing tasks. The company provides access to these high-powered chips—primarily sourced from Nvidia—along with associated data center resources, charging customers based on capacity and usage.

This usage-based model means CoreWeave’s revenue primarily comes from cloud service fees, essentially selling compute time on its GPU clusters. Customers can scale their GPU usage up or down as needed, and some enter long-term contracts for reserved capacity. Initially, CoreWeave catered to niche GPU needs, such as visual effects studios rendering graphics, but its recent growth has been driven by AI and machine learning workloads in industry and research. Major tech companies—including Meta, IBM, and Microsoft—have used CoreWeave’s infrastructure.

CoreWeave competes with major cloud providers like Amazon AWS and Microsoft Azure in delivering on-demand AI computing. However, its market positioning is that of a specialized alternative: its data centers are purpose-built for AI, which the company claims provides an edge in efficiency and performance for those tasks. Unlike generalized cloud providers that support a broad range of IT services, CoreWeave focuses exclusively on AI and GPU workloads. It has developed proprietary software, including the SUNK orchestration system and Tensorizer optimization tools, to maximize GPU utilization across clients.

As of December 31, 2024, CoreWeave operates 32 data centers running more than 250,000 GPUs, supported by 360 MW of active power. These data centers are part of a distributed network interconnected by low-latency connections to major metropolitan.

This specialization allows CoreWeave to rapidly deliver large-scale GPU capacity, a strength underscored by its close partnership with Nvidia. Nvidia has not only invested in CoreWeave but also supplies it with hardware—CoreWeave was among the first cloud providers to deploy Nvidia’s H100 and H200 GPUs upon release.

In short, company generates revenue by offering high-performance cloud computing services tailored for AI and other GPU-intensive workloads, monetizing its infrastructure through usage fees and enterprise contracts.

Financial Highlights

CoreWeave’s S-1 reveals explosive revenue growth alongside significant spending as the company scales. Key financial highlights include:

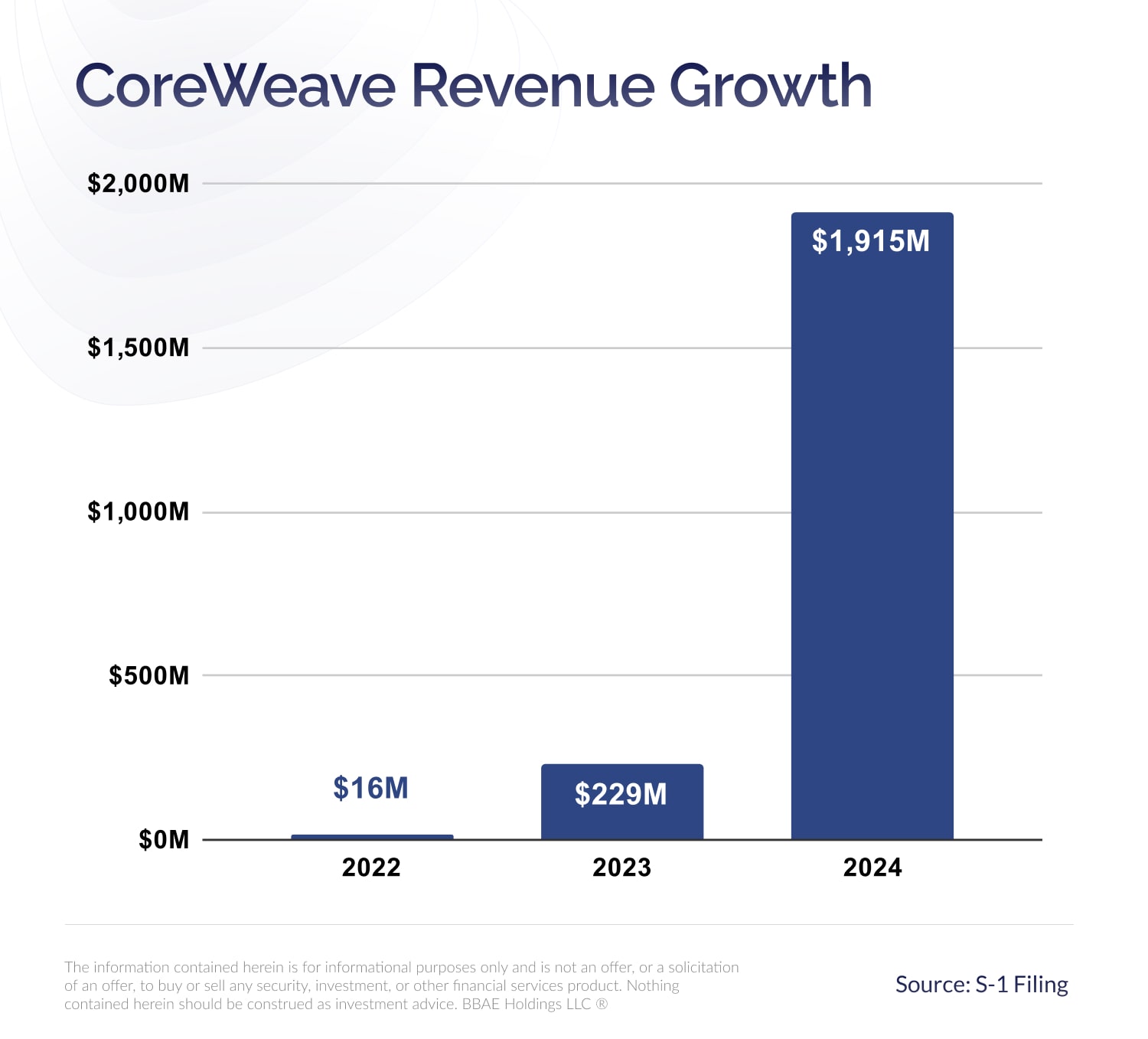

Soaring Revenue: Annual revenue surged from approximately $16 million in 2022 to $229 million in 2023, then skyrocketed to $1.92 billion in 2024. This represents 737% year-over-year growth in 2024, driven by the booming demand for CoreWeave’s AI-focused cloud services. Such rapid expansion is rare—what was a relatively small business just two years ago has evolved into a nearly $2 billion revenue company.

Major Customers: A significant share of CoreWeave’s revenue comes from a few large clients. In 2023, Microsoft was its biggest customer, accounting for 35% of total revenue. By 2024, Microsoft’s share grew to 62%, underscoring its deep reliance on company’s infrastructure. The company’s top two customers contributed 77% of total revenue in 2024, suggesting that Microsoft and another major client—possibly an AI firm—dominate its income.

In March 2025, CoreWeave signed a Master Services Agreement with OpenAI, securing a major long-term contract. Under this agreement, OpenAI has committed up to $11.9 billion in payments through October 2030 in exchange for cloud computing capacity. To fulfill this deal, CoreWeave agreed to create a special purpose vehicle (SPV) to manage the infrastructure supporting OpenAI’s workloads. As of March 11, 2025, the SPV was established, with agreements being finalized.

Additionally, as part of the deal, CoreWeave will issue OpenAI $350 million worth of common stock at its IPO price.

Profitability and Losses: Despite its surging revenue, CoreWeave is not yet profitable, as it continues to invest heavily in expansion. According to its S-1 filing, net losses widened from $593.7 million in 2023 to $863.4 million in 2024. These losses are primarily driven by massive infrastructure investments, equipment depreciation, and interest expenses on debt. In short, CoreWeave remains in a high-growth, heavy-investment phase, prioritizing expansion over short-term profitability.

Conclusion

The exact date and size of CoreWeave’s IPO have not yet been disclosed, but a November Reuters report suggested the company is targeting a $35 billion valuation.

Company’s S-1 showcases a company experiencing explosive growth in one of the fastest-evolving tech sectors. However, it also faces significant risks—including heavy reliance on a single major customer and supplier, competition with tech giants, and the challenge of managing large-scale investments and operations as it continues to scale.

Whatever the outcome, CoreWeave’s IPO is set to be one of the most highly anticipated of 2025.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investments involve inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Investing in initial public offerings (IPOs) carries additional risks, such as volatility, limited operating history, lack of liquidity, and potential overvaluation. IPO stocks may experience significant price fluctuations and may not perform as expected. Always conduct thorough research or consult with a financial expert before making any investment decisions. BBAE has no position in any investment mentioned.