2025 Investing Resolutions

Silly articles can be the most meaningful.

What I’m about to present – my final missive in my time as BBAE’s Chief Investment Officer – isn’t deeply acadmic. Rather it’s the type of advice I’d give to my son. A few points of advice to start him, or anyone, off on the right foot investing.

They can be New Year’s resolutions for 2025, or for any year.

New Year’s Investing Resolutions

- I will match my investment expectations with my investment time horizon.

If you’re baking a cake that’s going to take an hour, do you check it every 5 minutes and consider adjusting the temperature with every check? No. At least not unless you’re weird. Ditto for planting a seed that takes a few weeks to sprout.

In the physical world, shortchanging things that have an obvious, visible maturity cycle looks silly. But in investing, we do it all the time, and it’s one of the biggest killers of investment performance.

If you’re buying stocks with the expectation of holding for 5, 10, or more years, you’d best think long-term with both your expectations and how you measure the stock against them. The risk to avoid is being too jumpy – which, according to academic research – is exactly what most equity investors are.

- I will remember that stock picking is really hard before I begin picking stocks.

Picking stocks? Hey, as someone who ran a (market-beating) advisory service for 10 years, I’m spiritually with you. Just know that the odds are against you – strongly.

A small number of stocks (and a few slivers of time) do almost all the lifting. Michael Mauboussin found that from 1920 until present, 2% of stocks have created 91% of stock market wealth.

If you’ve been reading this blog for a bit, you’ve heard me talk about how Arizona State University professor Hank Bessembinder found that from 1924 to (roughly) present, just 3.2% of stocks contributed all of the US market’s returns, with the returns of the remaining 96.8% of stocks collectively matching Treasuries. (Incidentally, 60% of US stocks have lost money and 40% have gone to zero.)

Failure rates for picking long-term winning stocks round to 100% if we use crude enough numbers.

Sub-thought: AI could make picking stocks harder, not easier

As a bonus thought here, AI may make stock picking harder, in that LLMs can quickly do the work of standard equity analysts, meaning basic fundamental analysis could be becoming even less of a differentiator than it’s already become (in the old days, looking at financial statements and doing analysis was a differentiator because it was a skill that few possessed). See Larry Swedroe’s write-up in Alpha Architect’s blog about a paper (Shaffer and Wang, 2024) examining this.

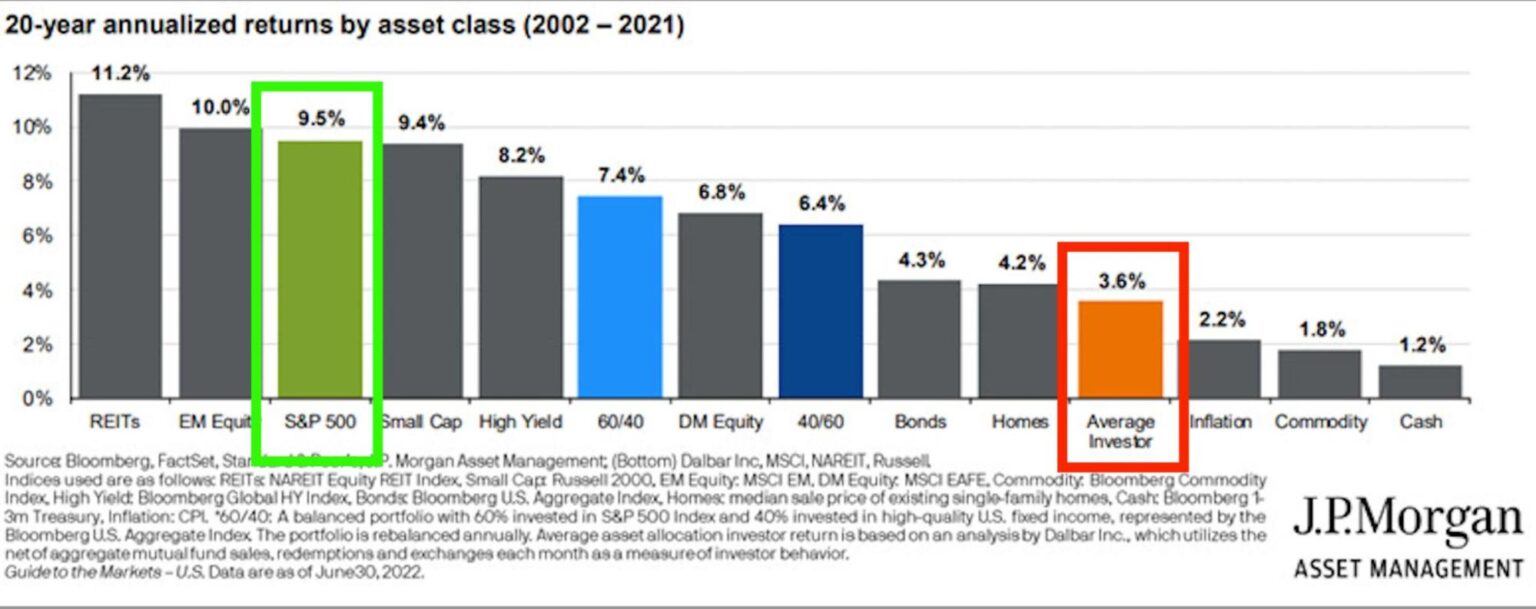

- I will try like heck to not be an average investor, because average investors perform terribly

Ned Davis Research and JP Morgan among others have done research into this, and it’s not pretty: People are too confident and too active, generally speaking (confidence likely fuels activity).

It’s ironic because generally, people are supposed to be pretty lazy, and buying and passively holding a low-cost index fund is literally the laziest way to invest. But almost nobody does it. Exact numbers vary by time period, but both Ned Davis and JP Morgan have found that average investors only earn about ⅓ of the returns available to them via “lazy” passive indexing.

People trade too much and overestimate (significantly) their stock picking ability.

Source: JP Morgan

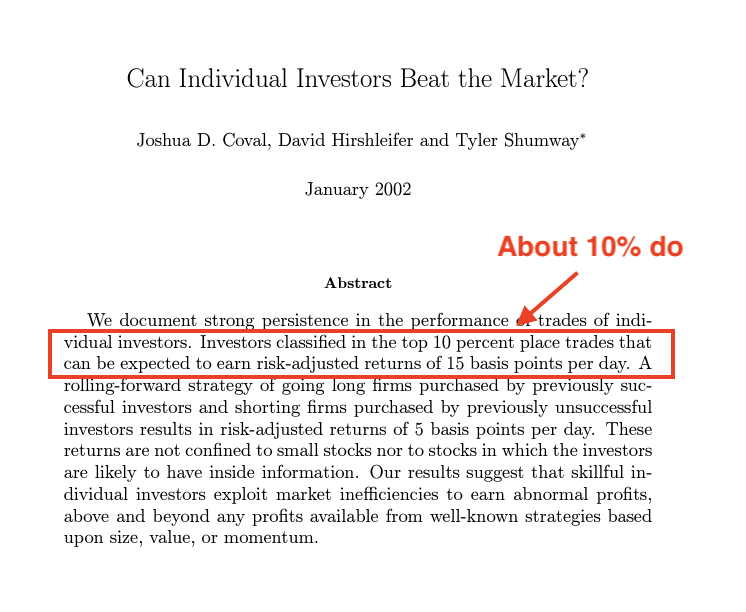

In fact, one study showed that just 10% of individual investors beat the market. It’s much easier to “be” the market (or at least own it) than to beat the market.

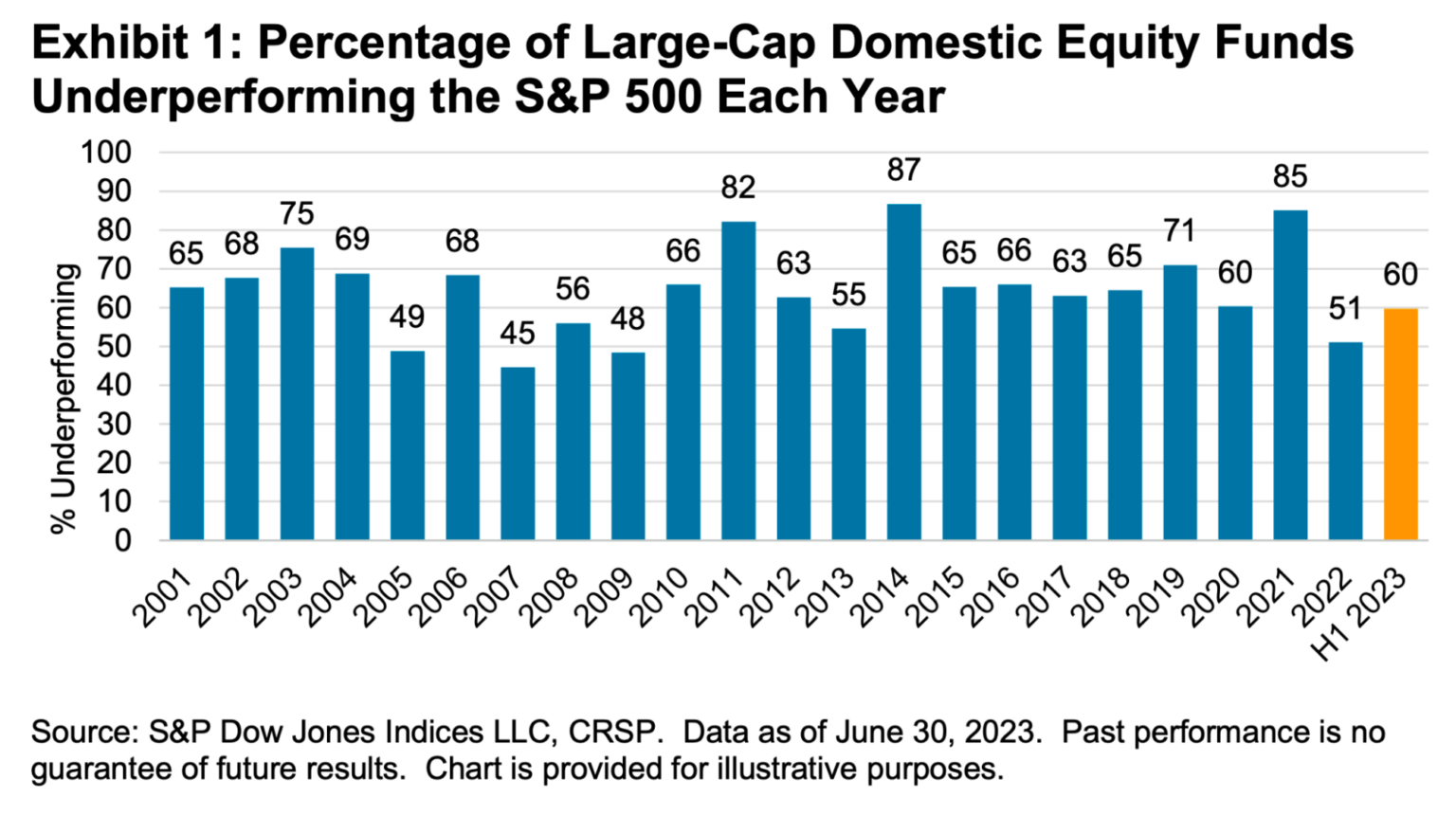

- I will remember that 94% of large-cap domestic fund managers lose to the S&P 500 over any 20-year period (85.6% underperformed over any given 10 years).

Individual investors almost never beat the market, and it turns out that professional investors aren’t very different. For any given year, the S&P Dow Jones Indices graph below shows that with only two exceptions (and then, barely), most US large-cap managers fail to outperform a simple index fund. As a rule of thumb, avoid active management unless you think you have a very good reason not to.

- I will not time the market, because timing the market is even harder than picking stocks.

Think picking stocks is hard? Timing the market is even harder.

JP Morgan found that if you’d missed the best 1.2% of trading days in the S&P 500, your returns would be 93% lower. Conversely, if you’d missed the worst 1.2%, your returns would be 2,150% higher.

Look, I know you’re special. But are your powers really magical enough such that you can jump into your assets of choice for “just the good days” and get out in time to avoid drops? Over the years I’ve met various clowns investors who claim to have some market timing system that would have worked in the past. Good for them, but reality says that timing the market is hard to do.

There are plenty of other resolutions, or at least lessons, I could have added to this list. Here are a few bonus mentions:

- Being mentally prepared for downs (academic evidence shows people bail on stocks prematurely, to their detriment); the S&P may have risen 9% or 10% on average historically, but its average intra-year decline since 1980 is – get ready for this – 14.2%. The intra-year decline is bigger than the average return – but to be clear, the average return is the real, final end result. That drop is just something investors need to stomach along the way, so the better at stomaching drops you can cajole yourself to be, the better investor you’re likely to become.

- Ignoring price targets and price target-y forecasts. They’re done by smart, well-trained and well-resourced people, but they’re also a joke. Much of what derails people about investing has to do with misapplying the idea that investing (being numerical) is a numerical science. It’s really a social science underneath, in that its manifested reality doesn’t come from numbers, but from human decisions. Numbers just describe the results.

- Running with the “social science” theme, recognizing that cognitive biases are our truest enemies in investing. Framing bias, loss aversion, herd instinct, recency bias – there are many more. It’s not easy uncovering our blind spots in life because, well, by definition we don’t see them. But either a pre-investment decision mental checklist (ideally) or at least reading about these biases and thinking about them in regard to your own investing will pay dividends, figuratively and perhaps literally, too.

- And not a suggestion or resolution, but perhaps a think to look out for: AI may make st

Happy investing in 2025. It’s been great having you as a reader and I wish you success – in both investing and in life.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.