Klarna ($KLAR) IPO: Everything You Need to Know

Klarna, the Swedish fintech known for popularizing ‘Buy Now, Pay Later’ (BNPL) services, has finally pulled back the curtain on its much-anticipated U.S. initial public offering. The company’s Form F-1 (the S-1 equivalent for foreign issuers) filing reveals a story of rapid growth and recent financial turnaround. In this article, we will cover the key IPO details investors need to know.

Company History

Klarna was founded in Sweden in 2005 by Siemiatkowski, Adalberth, and Jacobsson with the goal of simplifying online payments. By 2010, it had expanded across the Nordics and entered Germany and the Netherlands. Between 2014 and 2015, Klarna launched in the UK and U.S., marking its first expansion beyond Europe. In 2017, it secured a Swedish banking license, broadening its services beyond BNPL to retail banking.

The pandemic-driven e-commerce boom in 2020 and 2021 propelled Klarna’s valuation from $5.5 billion to $45–46 billion, making it Europe’s most valuable fintech startup. This surge was part of a broader trend in the BNPL sector, where valuations skyrocketed across the industry. A key milestone was Square Inc.’s (now Block Inc.) $29 billion acquisition of Afterpay in August 2021, highlighting the sector’s explosive growth. However, in 2022, rising inflation and interest rates triggered a fintech downturn, cutting Klarna’s valuation to $6.7 billion. Facing heavy losses, the company shifted focus to cost-cutting and operational efficiency. By 2023, the company had tightened credit underwriting, neared breakeven, and regained a valuation in the mid-teens of billions. In 2024, it reported its first annual profit and confidentially filed for an IPO in November, followed by a public F-1 filing in March 2025.

Business Model & Revenue Streams

Klarna’s business revolves around offering consumers flexible payment options at both online and offline checkouts. Shoppers can split purchases into interest-free installments or defer payments for a short period without fees.

How Klarna Makes Money

Unlike credit card companies that rely on consumer interest and fees, Klarna’s revenue comes primarily from merchants. When a shopper uses Klarna, the retailer pays a small percentage of the transaction (a merchant discount fee). In exchange, the company takes on the risk and responsibility of collecting payments from the consumer. Merchants accept these fees because Klarna increases sales and reduces cart abandonment. About 99% of Klarna’s transactions are interest-free for consumers, prioritizing high transaction volume over interest revenue.

For longer-term financing (marketed as “Fair Financing”), Klarna may charge interest or fees, but this accounted for just 1% of total volume in 2024. The company funds its BNPL purchases through a mix of external credit facilities and its Swedish banking license, which allows it to use customer deposits—giving it a cost advantage over non-bank competitors that rely on expensive debt. Klarna’s proprietary underwriting technology, increasingly powered by AI, assesses risk in real-time to approve consumers quickly while minimizing defaults.

Beyond Payments: Klarna as a Commerce Platform

Klarna has evolved beyond a simple payment service into a broader commerce platform. Its shopping app enables users to browse deals, track deliveries, and earn rewards. The company has also built a retail media business, where merchants pay to promote their products to Klarna’s massive user base, similar to an affiliate model. The company describes this as “a unique advertising solution connecting engaged consumers to advertisers in a personalized, commerce-centric environment.”

Additionally, Klarna has expanded its ecosystem with the Klarna Card (available in select markets) for in-store BNPL purchases and integrations with Apple Pay and Google Pay for seamless transactions. The company aims to be an “everyday spending and saving partner”, offering not just financing but a one-stop app for shopping, payments, and savings. In the U.S. and parts of Europe, Klarna has introduced high-yield savings accounts, attracting deposits that further fuel its lending operations.

Revenue Growth & Profitability Trends

Klarna’s revenue has been growing at a strong pace. In 2024, it reached $2.81 billion, up 24% from $2.28 billion in 2023. This growth was fueled by higher payment volumes (GMV), an improved take rate, and rising advertising and affiliate revenue. The company’s aggressive expansion in the U.S., its fastest-growing market by 2024, also played a key role. For perspective, its revenue in 2021 was just $1.1 billion, meaning Klarna has nearly tripled its revenue in three years—a testament to the global adoption of the BNPL model.

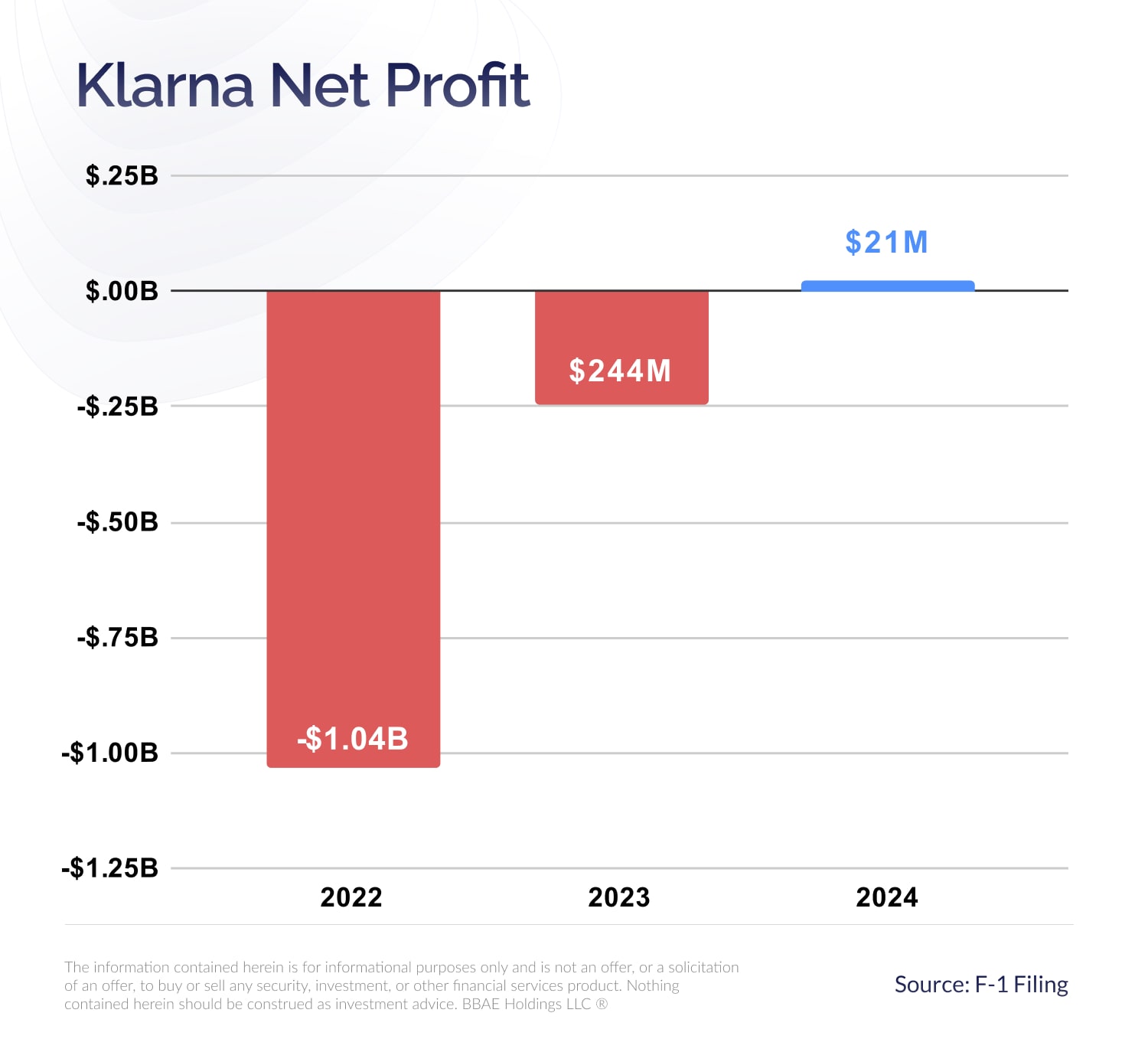

Perhaps the biggest shift in Klarna’s IPO filing is its profitability turnaround. The company posted a $21 million net profit in 2024, a significant reversal from a $244 million loss in 2023. Just two years earlier, in 2022, the company had lost nearly $1 billion, after heavy spending on expansion and rising credit losses during the downturn. The 109% improvement from 2023 to 2024 highlights the success of Klarna’s restructuring. Cost-cutting measures, including layoffs and efficiency improvements, along with better credit performance, helped push the company into profitability.

Below is a breakdown of Klarna’s financial trajectory from 2022 to 2024:

Source: SEC Filing

Other Key Metrics

According to Klarna’s S-1 filing, the platform had 93 million active customers by the end of 2024 and processed an average of 2.5 million transactions per day. These figures highlight the scale driving its financial performance.

Klarna’s gross merchandise volume (GMV)—the total value of transactions processed—reached $105 billion in 2024, up from $92 billion in 2023 and $83 billion in 2022. For context, the company’s GMV was $35 billion in 2019, meaning it has nearly tripled in five years, reflecting the widespread adoption of BNPL.

At the same time, Klarna’s take rate—revenue as a percentage of GMV—has steadily increased from 2.3% in 2022 to 2.7% in 2024, as the company monetizes more services per transaction.

Klarna and AI

AI is central to Klarna’s operations—mentioned 207 times in its F-1 filing, the company even describes itself as an “AI-powered” business.

The company has integrated AI across its business, significantly enhancing efficiency and reducing costs. According to the company, its AI-powered assistant, developed in partnership with OpenAI, now handles 62% of customer service chats, saving an estimated $39 million in 2024—the equivalent workload of over 800 full-time agents. AI has also optimized internal processes, such as automating case log classification for engineers, which alone contributed $4.8 million in savings.

Beyond operations, AI improves merchant conversion rates, personalizes shopping experiences, and enhances underwriting accuracy, driving both revenue growth and operational efficiency. These AI-driven improvements have been instrumental in reducing the company’s operating expenses as a percentage of revenue by 47 percentage points from 2022 to 2024, while GMV grew by 27%. Collectively, these efficiencies led to an $859 million improvement in operating results and a return to profitability in 2024.

Conclusion

Klarna’s IPO is set to be one of the most significant fintech debuts in recent years. However, its F-1 filing has yet to disclose the number of shares or price range. The company has applied to list on the New York Stock Exchange (NYSE) under the ticker symbol “KLAR.” Pricing details are expected to be announced in the coming weeks.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investments involve inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Investing in initial public offerings (IPOs) carries additional risks, such as volatility, limited operating history, lack of liquidity, and potential overvaluation. IPO stocks may experience significant price fluctuations and may not perform as expected. Always conduct thorough research or consult with a financial expert before making any investment decisions. BBAE has no position in any investment mentioned.