Leveraged ETFs: Should You Buy Them and Hold?

Bloomberg’s Matt Levine referenced a Bloomberg article by Katie Greifeld (registration may be required) discussing the weird performance of a GraniteShares product offering three times the daily return of MicroStrategy – a highly volatile company that’s become a de facto bitcoin proxy bank thanks to Executive Chairman Michael Saylor’s crypto leanings.

From Katie:

“While MicroStrategy itself is higher by more than 100% this year, LMI3 has dropped nearly 82%”

On the surface, it seems odd that a fund that’s supposed to triple a stock’s return – which would mean 300%+ returns for a stock that went up 100% – instead declined by 82%, thus underperforming the underlying it’s tracking by 182%.

Actually, this is according to plan.

And it’s not an occurrence unique to MicroStrategy. From a 2008 Wall Street Journal article:

“…Even more confusing, the ProShares fund designed to return twice the opposite of the Dow Jones U.S. Real Estate Index was down 50% for 2008, while the index was also down, by 43%.”

What’s going on with leveraged ETFs? Let’s unpack – and see why their longer-term performance isn’t always so bad.

How leveraged ETFs work

If you know about leveraged ETFs (GraniteShares’ LMI3 is technically an exchange traded product, but same idea for this level of discussion), you know that they’re designed to give you some derivative (2x, 3x, -2x, whatever) of the daily performance of an underlying asset – most commonly an index, but these days, sometimes popular individual stocks, too.

You might also know that because leveraged ETFs generally reset or rebalance daily, that 2x or 3x performance literally just applies one day at a time, and that longer-term returns can be wildly different from the underlying, as with the GraniteShares MicroStrategy ETP, even if those in the know are fully OK with this.

Leveraged ETF decay, as the negative side of this divergence is termed, happens for two broad reasons:

- Volatility Drag: Ever heard the investing saying that a 50% drop requires a 100% gain to break even? You understand volatility drag. Because of the way compounding works, downward-trending and even horizontally trending volatility eat into leveraged ETF (and ETP, but I’ll just say “ETF” for shorthand) returns more than you might think. There’s a path dependency to leveraged performance, too: A series of magnified downward movements can dig a hole that’s really hard to climb out of. If the underlying drops by, say, 30%, it needs to rise by 42.8% to break even. But if a 3x ETF drops by 90%, it needs to rise by 1,000% to do the same.

- Buy-high-sell-low rebalancing mechanics: Leveraged ETFs provide you leverage by using leverage themselves, which has a cost, but more generally, because they need to maintain a certain ratio of stock to leverage (which may be literal borrowings, or futures contracts), when the underlying rises in price, they need to buy more of it, and when it falls in price, they need to sell some. Buying more when prices rise and selling when prices drop is the opposite of what we’re taught to do in investing.

“Decay” sounds scary, and like the kind of thing that would be easy to misunderstand. So the SEC has written warnings on leveraged ETFs – here’s one from 2023 – and the media hasn’t been kind to them, either:

So are leveraged ETFs and ETPs for imbeciles? No. They are for day traders. Whether or not day trading is good is a separate discussion, but the companies, to their credit, are generally clear about the intended users, and do a careful job of suggesting investors not hold these leveraged products for the longer term – even if not every investor reads the label.

But most do.

Matt’s Bloomberg friend Katie notes that the Direxion Daily TSLA Bull 2X Shares ETF, for example, turns over its holding every 3.5 days (versus 185 days for VOO, the regular, non-leveraged Vanguard S&P 500 ETF), meaning investors are, as intended, using leveraged ETFs (or at least this one) pretty much for day trading.

Matt celebrates this:

“Anyway the good news is that (1) these products are fun and (2) people seem to understand that they are not buy-and-hold products.”

But what if someone wanted to buy and hold leveraged ETFs anyway?

The short answer is that it’s hard to generalize, is wildly volatile to the point your investment could be wiped out, and performance depends greatly on the exact timing of your investment(s), but despite all that, leveraged ETFs can offer some pretty amazing buy-and-hold returns.

A good LinkedIn article by Christian Knapp of Bosun Asset Management makes the case that leveraged ETFs have been unfairly maligned as long-term investments. This article is a bit too positive in my view, in that I’d like to see more performance during really nasty time periods examined, but Christian makes a fair point in this example:

“Let’s look at SSO (2X the S&P 500 on a daily basis) as an example. Examining it from its inception in June 2006 through late December 2022, we see a cumulative return of 404%. This is far higher than its non-leveraged counterpart, SPY, which returned 209%.”

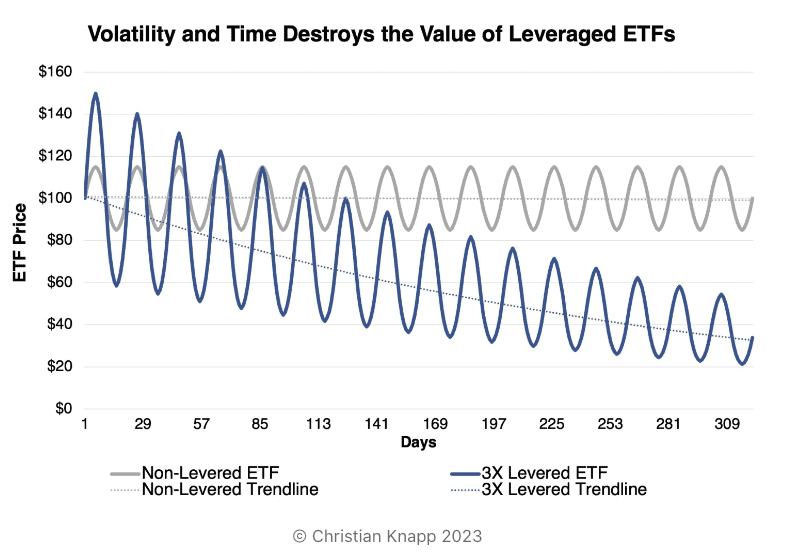

And he shows a graph illustrating that even during a “flat mean” period of volatility – volatility that nets out to zero, despite ups and downs – the leveraged ETF (blue squiggle) underperforms the regular ETF (gray squiggle).

So like a sinking ship, leveraged ETFs are destroying your wealth if you’re buying and holding them without an upward trajectory in the underlying asset.

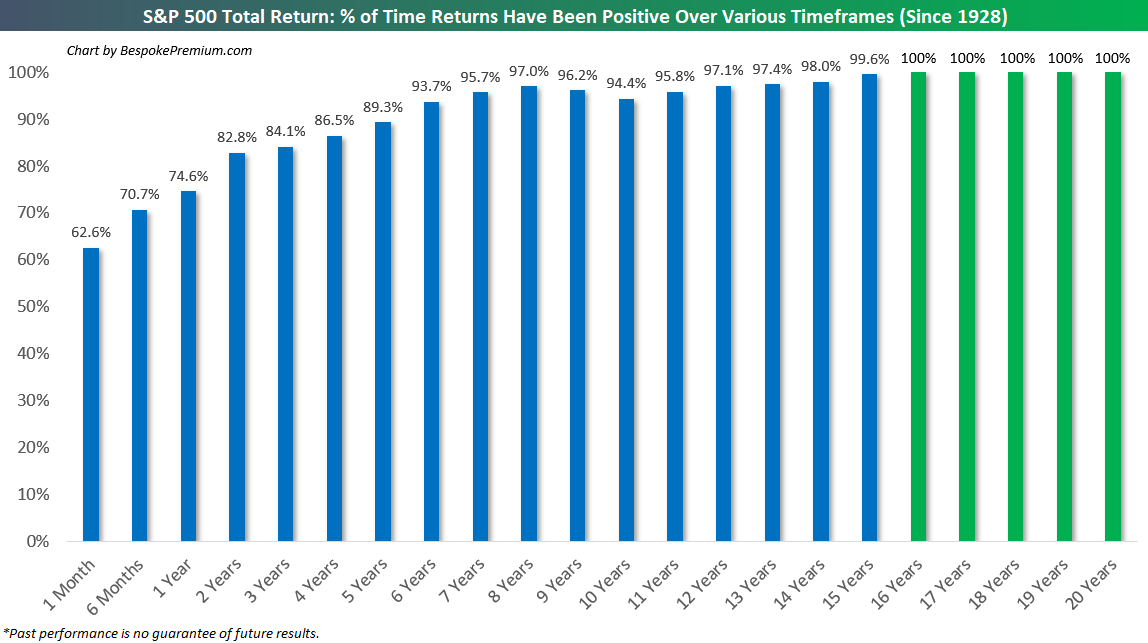

But doesn’t the stock market usually go up? Loyal BBAE Blog readers know that it has over time, and reliably so:

Source: Bespoke Investment Group

Therefore, it shouldn’t be taboo to wonder if, despite the “day trading only” warnings on the package and despite the fact that leveraged ETFs can produce counterintuitive returns patterns and have higher-than-average fees, whether you’d actually be OK if you held on for a really long time as long as the underlying asset goes up over that really long time.

Well, the answer depends on your definition of “OK,” but speaking solely for an ETF tracking the US S&P 500, you could have made a ton of money.

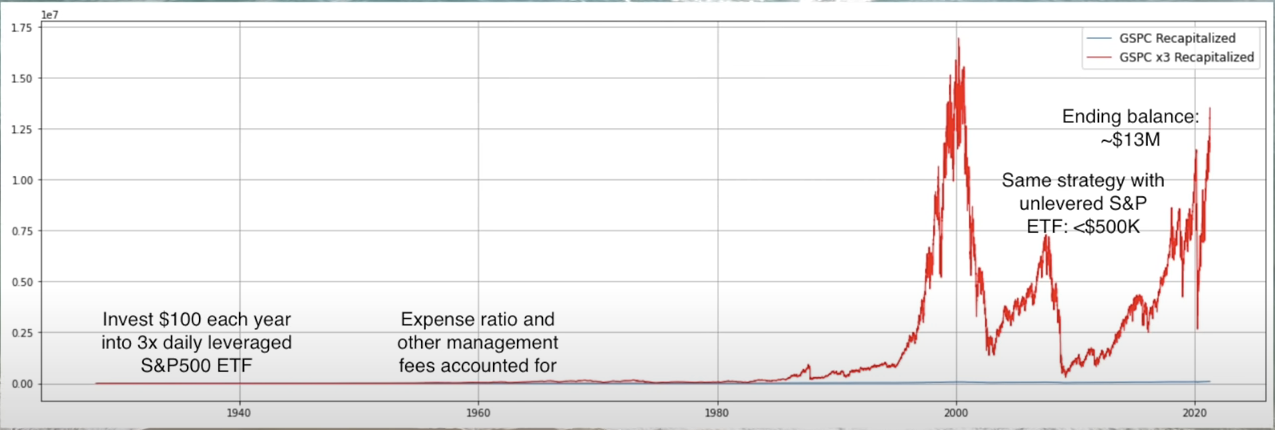

I’m going off of computations from one “Wall Street Millennial” who made this video regarding a simulation he ran of a hypothetical 3x S&P 500 ETF going back to 1927.

Before you get excited, consider his warning: The returns are highly dependent on when you originate a position.

He also points out that had you put a lump sum in at the wrong time, buying a 3x leveraged ETF “would have bankrupted you” around the Great Depression. If you’d had the luck to buy at the right time, your returns would be mind blowing.

But his most true-to-life results come from backtesting dollar cost averaging, because that’s more akin to how real people invest over long periods, and has the side benefit of “time diversification,” which is especially important with frenetically gyrating leveraged ETFs.

Wall Street Millennial simulated a $100 investment into a 3x leveraged S&P 500 ETF every year since 1927. It was a wild ride, but ended up massively outperforming the regular market, whose results look flat (blue line) in comparison.

The hypothetical 3x ETF would have left an investor with $13 million – versus less than half a million from the regular S&P 500.

Theoretical results of $100 invested each year from 1927 into an also-theoretical 3x leveraged S&P 500 ETF. Screenshot from a Wall Street Millennial video on YouTube

Of course, this is with the hindsight of knowing the market rose nicely from 1927. And for most people, 50 or 60 years is probably a maximum investing span – and that’s even assuming getting started young. That means that while the 100-year example is informative, it understates the risk to real-life investors who may need to tap their money during one of those horrific drawdown periods.

Counterpoint to the counterpoint

You’d rather have $13 million than $500k, and so would I, and I do think it’s reasonable to say that leveraged ETFs have been a bit unfairly maligned, or somewhat miscategorized, in the sense that they can offer an attractive – if wild – return potential if held long enough, and if the underlying is some sort of broad index that taps the overall economic progress that humanity, or at least American humanity, makes – like the S&P 500.

Considering that most stocks lose money, I would be far more cautious about single-stock leveraged ETFs as buy-and-hold investments.

Again and to be very clear, ETF companies aren’t billing leveraged ETFs as long-term holdings for at least some good reasons, and I don’t want to give the impression that a 3x (or 2x, or 1.5x) leveraged ETF is a “nest egg”-type investment for any investor.

Could investors really stomach holding a leveraged ETF for many years anyway?

In researching this piece, I stumbled across a subculture of leveraged ETF (LETFs, they’re called) aficionados. Not every post was reflective of deep understanding – those SEC warnings have their place – but in this Reddit thread, a user called BetweenCoffeeNSleep shared some relevant behavioral finance wisdom:

“…That’s why most people shouldn’t be long LETFs. The math is arguably over discussed. The human, psychological component is grossly under considered. People panic sell at a loss with 1x. Holding 2x or 3x through this kind of year can make it feel like there will never be an end. Reading the things people say about LETFs will make it far worse if you’re not prepared.

All of the above, if the positions are significant parts of your total asset allocation, are exponentially amplified.

These things move violently, and they will emotionally wreck unprepared holders.”

CoffeeNSleep is right.

Dalbar Research found that over a 20-year period when the S&P 500 itself rose 10%, the average US mutual fund investor earned just 4%, thanks to terrible timing – buying at highs and panic selling at lows.

If the average investor’s decision making degrades to squirrel-crossing-the-road level with just the boring S&P 500, imagine the emotional overload a 3x leveraged ETF could cause if bought and held.

So, yes, you can absolutely buy and hold leveraged ETFs for the long haul.

Would it be OK to test with a very small, “fun money” portion of your portfolio? Perhaps for some people, though I can’t tell you what’s right for you.

Should you do it with any serious portion of your portfolio? I don’t think anyone would recommend that. Leveraged ETF are best treated as creatures of the day.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.