Weekly Roundup: Cheap Small Caps, Kamala Harris Shouldn’t Change Your Portfolio, Beware of IPOs

Pricey markets – and are small caps cheap or expensive?

A recurring topic in these updates has been how pricey – or not – US markets currently are.

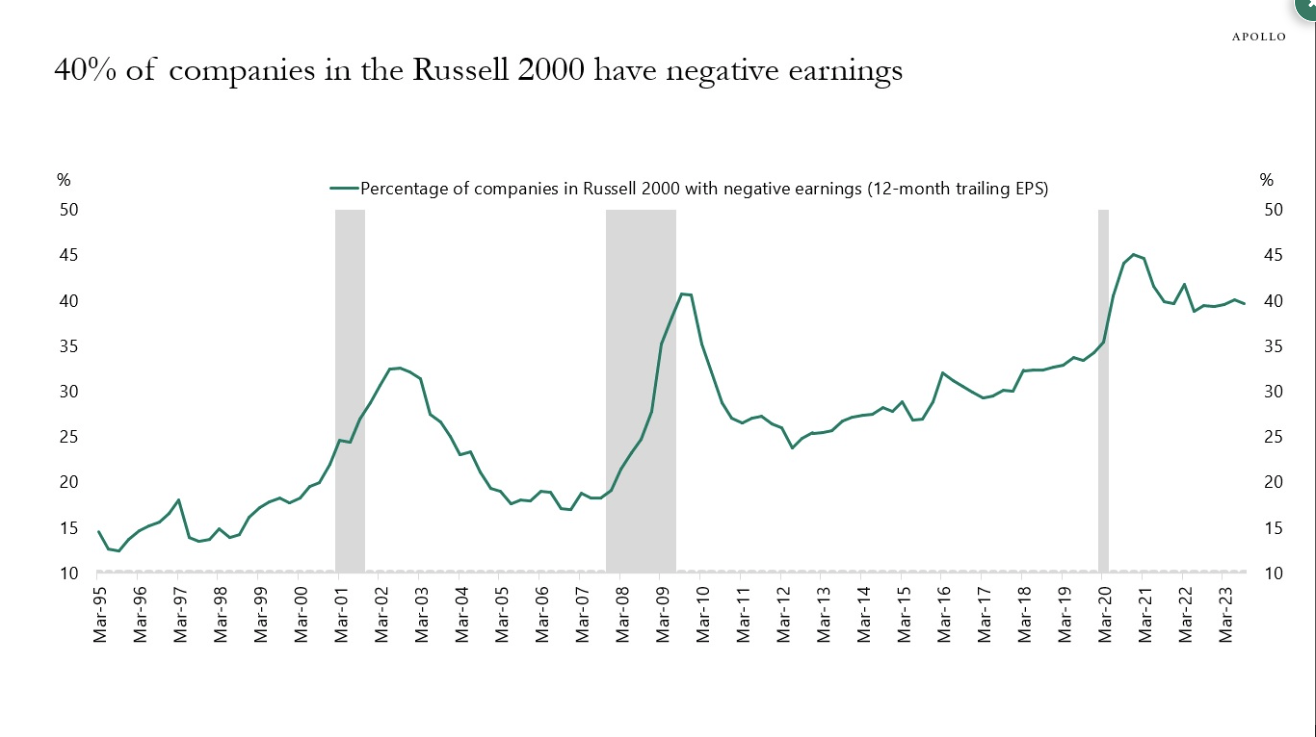

As you know if you’ve been a regular reader, the Dow Jones, S&P 500, and Nasdaq have all had different personalities lately – the DJIA set a record high on a day the Nasdaq 100 tanked last week – and that even within the S&P 500 (which embeds the Dow and Nasdaq 100 axiomatically), small caps have been mediocre performers, with earnings misses and soft earnings. In fact, 40% of small-cap Russell 2000 company earnings are currently contracting, per BlackRock, and last fall, 40% were losing money.

The money-losing-ness of small caps has actually been increasing over time:

I’m forgetting the percentage, but many small US companies are just barely covering their debt costs.

Large caps, though, have had it different: Whereas Russell 2000 earnings growth was -12% for the first quarter of 2024, S&P 500 earnings growth was 5.6%, and would have been 8.7% with health care excluded (numbers per Schwab). And most of the S&P 500 index isn’t even large cap stocks.

If there’s ever been a time that “the market” was an overgeneralization, now is that time.

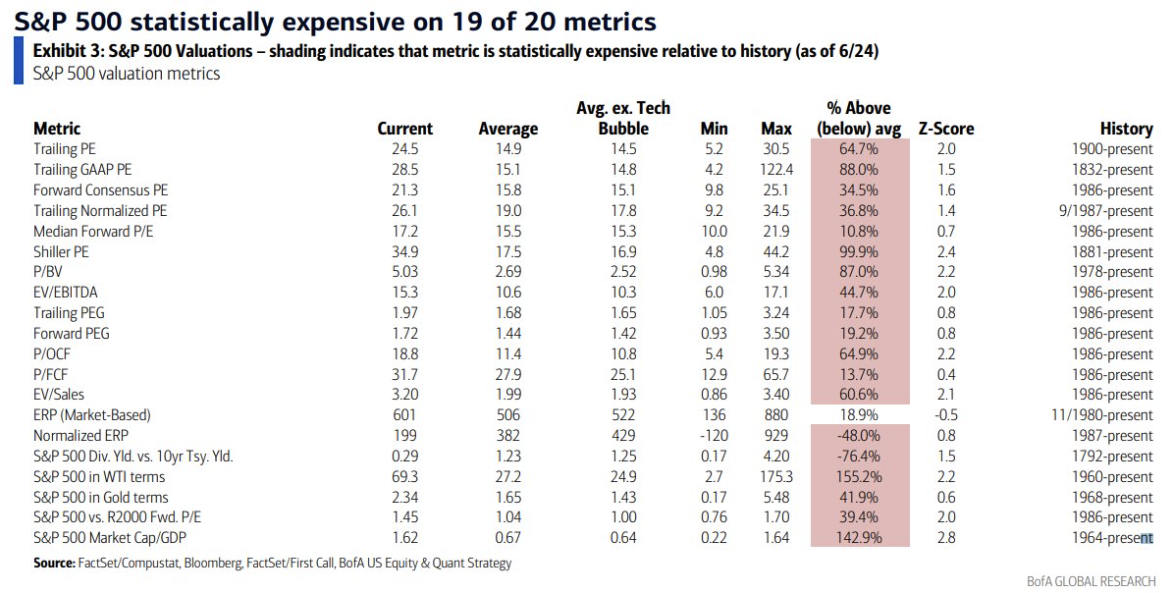

Anyway, the overall S&P 500 is looking pricey on a slew of metrics, per Bank of America Research:

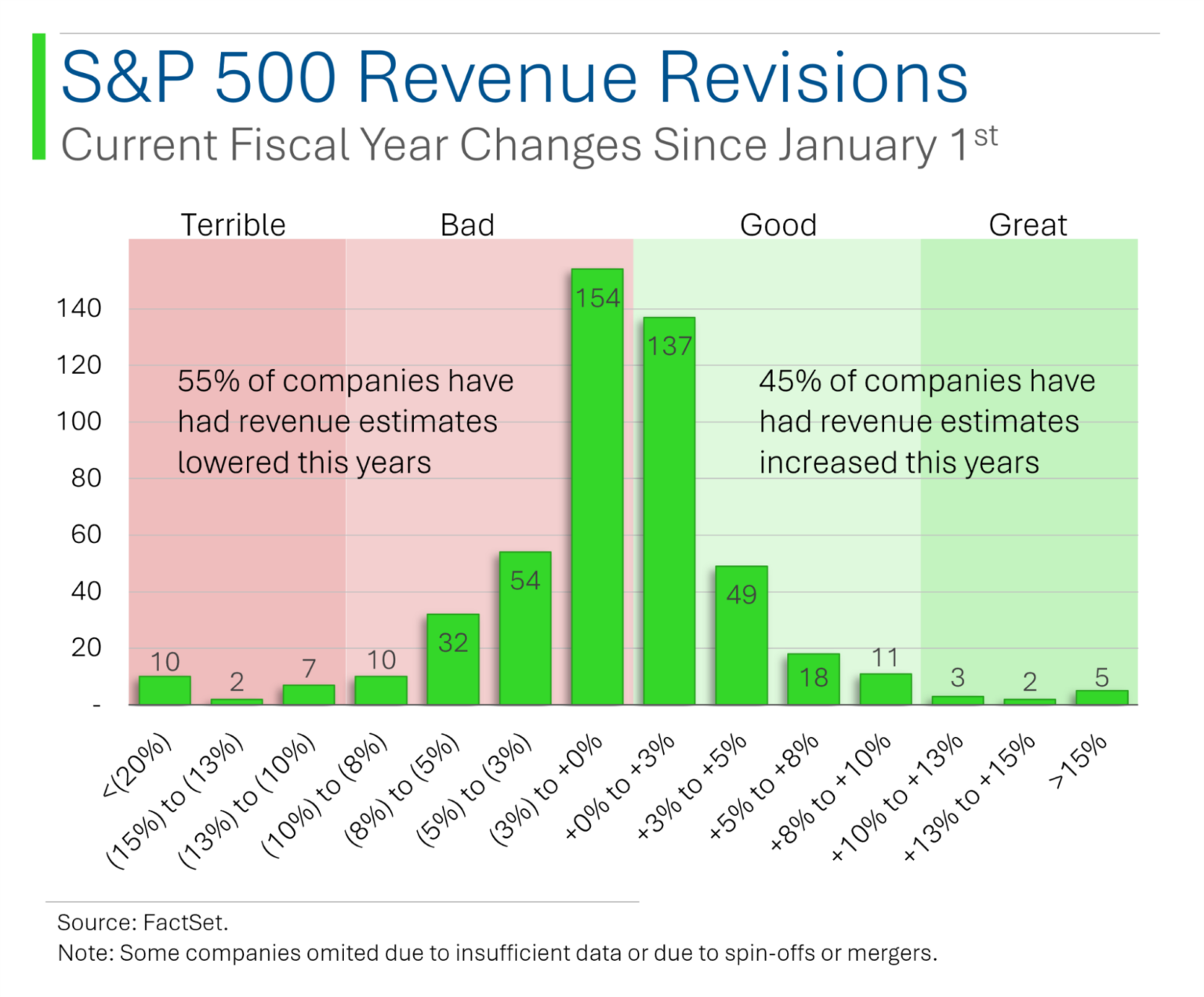

Adding to the top-heavy appearance of the S&P 500 is that revenue revisions are starting to lean downward:

Large caps: Priced to perfection. Small caps: Priced to surprise?

Meanwhile, Schwab expects the small-cap Russell 2000 to post a collective 20.7% earnings growth for 2024, versus just 9.9% for the S&P 500.

In other words, a reversal of fortunes could be in the making. But don’t quote me on that.

Don’t bet on politics (at least with your portfolio), for the 17th time

With Joe Biden now out of the presidential race, investment eyes are again turning to what the race – presumably with Kamala Harris as Democratic frontrunner, at least initially – means for markets.

This is understandable.

This is also one of the dumbest things to do.

As I’ve said in some recent BBAE Blog posts, politics can be hard to predict – not just elections, but the decisions of a handful of ruling people ongoingly. And often, political issues, because of their media visibility, often seem like bigger market movers than they end up actually being.

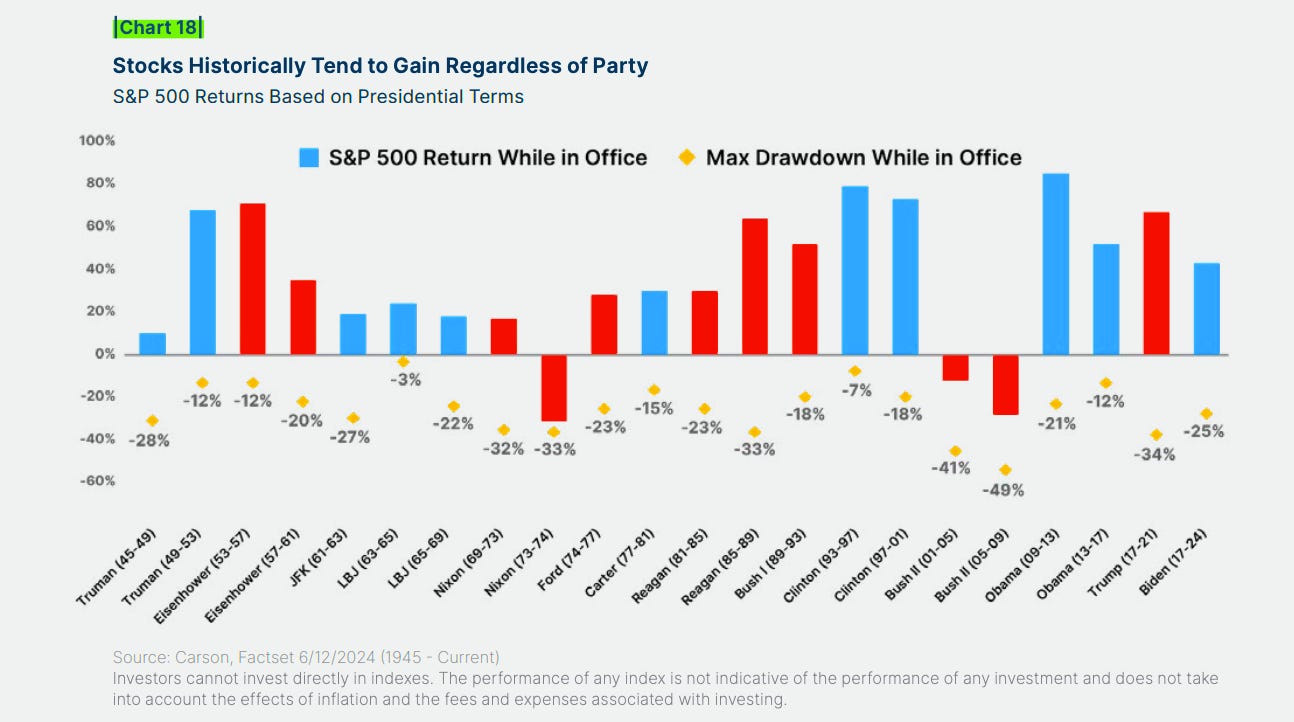

Roger Conrad, a superb energy analyst and friend of BBAE, said in a recent note that if you want to bet on politics, go to a prediction website. Otherwise, don’t focus on politics in your portfolio. Roger nails it below in this excerpt from his recent missive, noting how counterintuitive the market moves under both Trump and Biden were:

“The best performing S&P 500 stock sector since the Biden Administration took office is oil and gas, with twice the gain of second place Big Tech. Conversely, during the Trump years, the S&P Energy Index lost more than half its value.

Or take renewable energy: The largely earnings-less S&P Global Clean Energy Index was a huge Trump years winner, gaining over 150 percent and double the return for the S&P 500. Since Biden took office, that Index has lost more than half its value.

Clearly, investment performance had nothing to do with government policies, which have been quite aggressive the past 8 years. But even a focused government not afraid to push boundaries can only affect so much, including for businesses as politicized and therefore regulated as energy.

When Trump entered office in 2017, peddlers of politics based investing pounded the table to buy oil and gas stocks. They preached sector Armageddon in 2021 when Biden came to power, while advising the opposite for renewable energy stocks.

Each time, they got it exactly wrong—not because they misinterpreted what the Biden and Trump Administrations would actually do. Rather, they grossly over-estimated the impact of government action and so doing underestimated more important factors.”

Who would have predicted that?

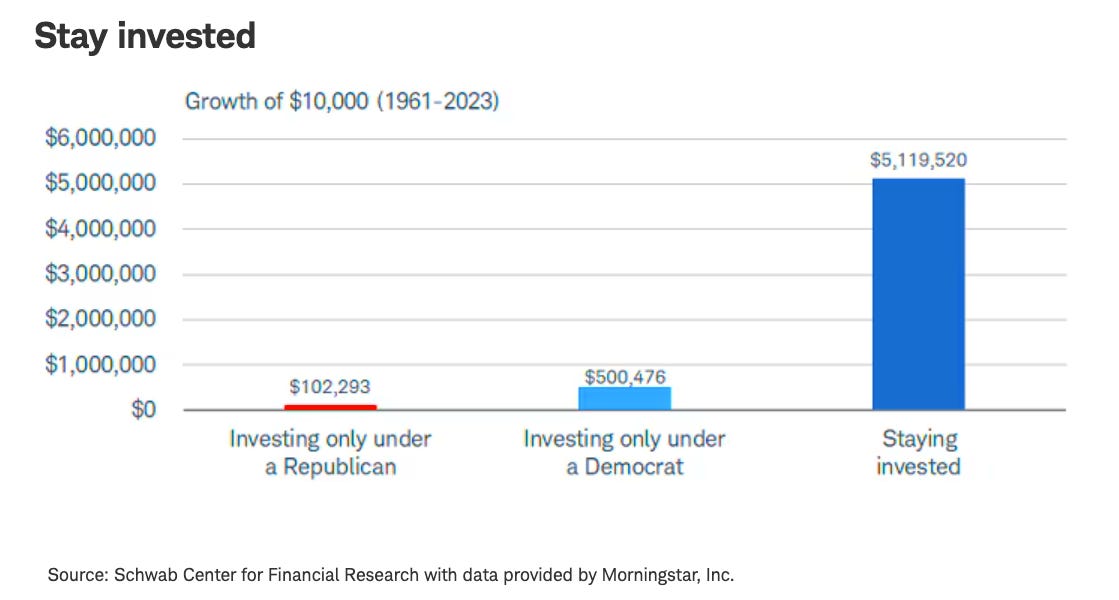

Sam Ro of Tker.co showed a few charts that illustrate the futility of administration-based investing:

It’s really tempting to invest based on politics. New administrations talk about changes, and do make changes. But there’s just not enough of a “signal” there, in mathematical parlance.

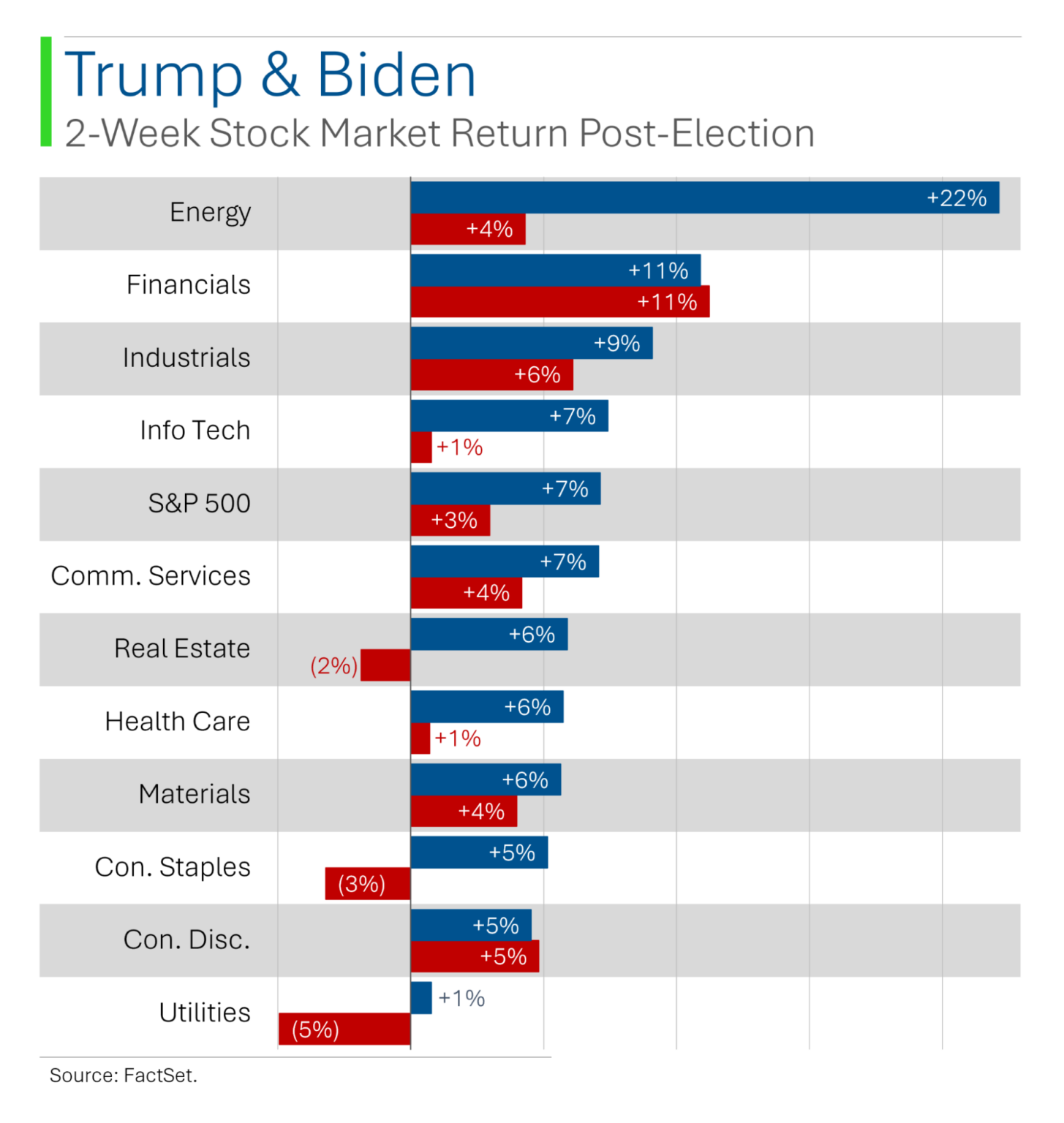

Another graphic Sam shared:

Now, if, for some weird reason, I absolutely had to invest based on politics, I’d take two paths.

The first, as I’ve mentioned in other pieces, is not election-based per se: I absolutely think it’s prudent to account for regulatory trends in the utility sector. Certain states are either more or less hospitable for utilities. But even then, the state regulatory agencies are not the sort of things that change entirely with new state political administrations. A softening regulatory agency could be a potential investment catalyst, because in the utility industry, the regulators determine how much money a utility gets to make. I’d actually consider this closer to regulatory investing than political investing, though.

The second would be a very short-term play that exploits post-election price movements. This type of investing has nothing to do with actual economics; it’s just a “second derivative” play on market reaction,

A graphic from StreetSmarts – again from the mysterious “Ryan” who’s talented with visuals – shows the two-week returns following both Biden (in blue) and Trump elections.

Note two things:

- These are huge bumps, generally. The market can clearly move on election news. I would have expected more movement with Trump’s election than Biden’s because the odds were strongly in Hillary’s favor, making Trump’s 2016 win more of a surprise.

- These moves are reminders of how anticipatory the market is. They’re just following elections. No inaugurations had happened yet, let alone any actual economic reality following new policies put in place.

But be careful: Just because the market may move after an election doesn’t mean those moves are predictable. In fact, if they were obviously predictable, the market would simply price them in.

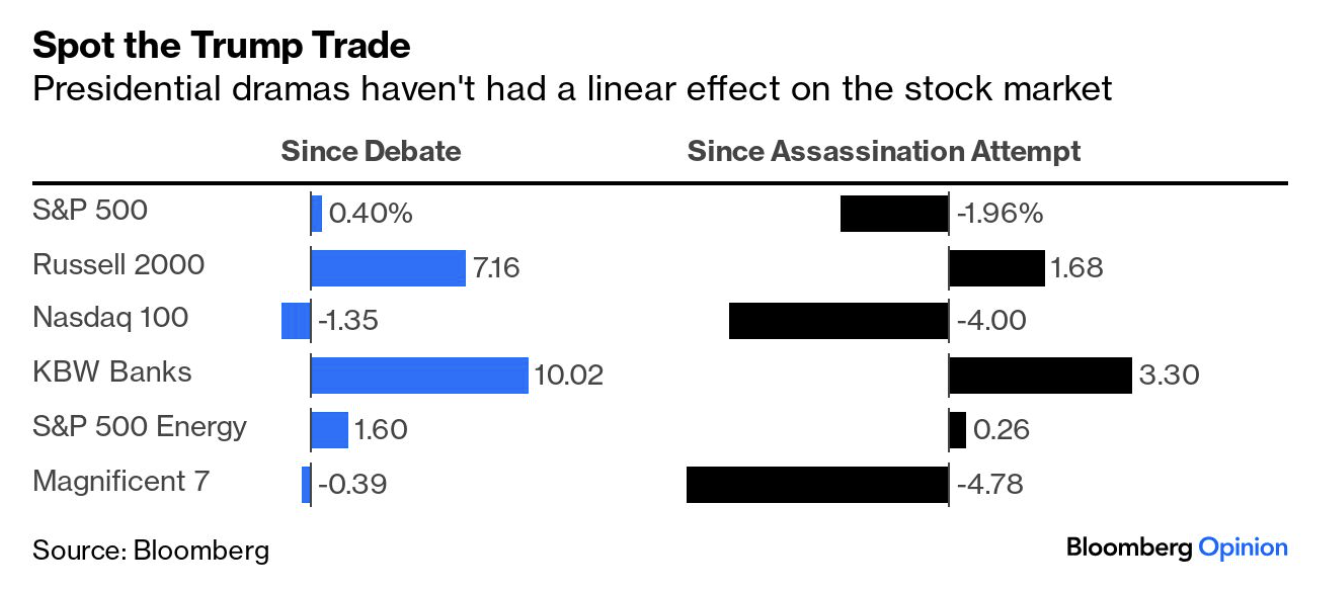

If my point still isn’t clear enough, see this graphic from Bloomberg, which shows essentially no clear pattern to price movements of various parts of the market.

Bottom line? Take all the content about investing based on presidential politics as entertainment, not as serious investment advice.

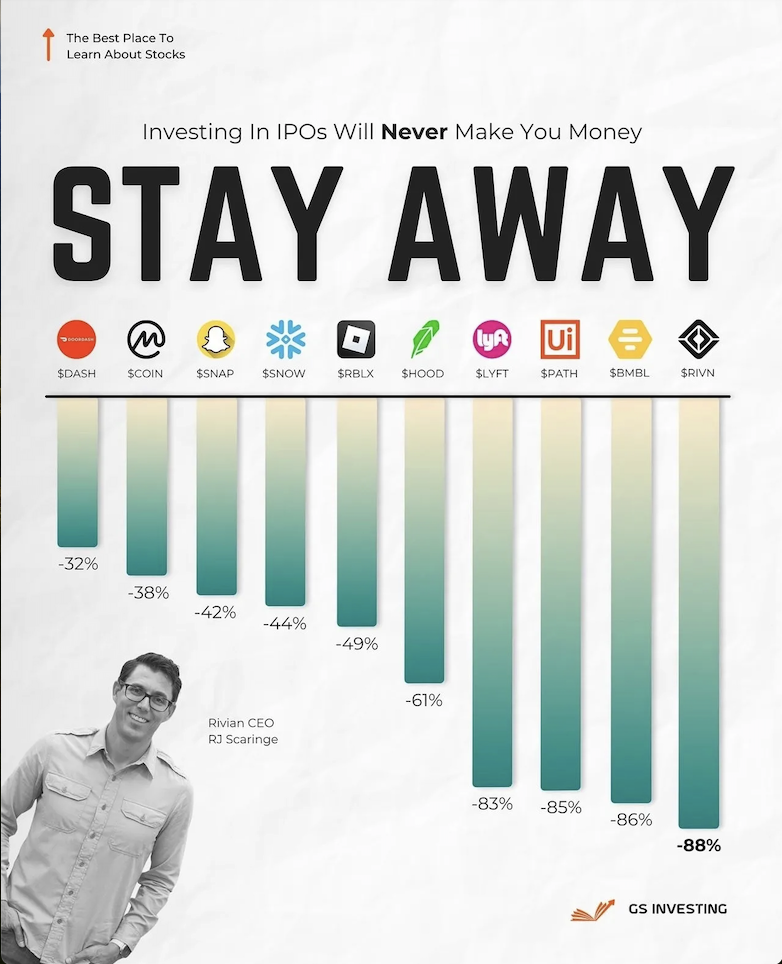

IPOs: Suckers’ bets (statistically)

I don’t read the GRIT newsletter often, but I spotted the below infographic in it, which shares a scary truth about initial public offerings (IPOs): They tend to not perform well.

Now, I deduct credibility points for overgeneralization: “Investing in IPOs Will Never Make You Money” is obviously untrue at face value, even if it’s directionally true.

The thing about IPOs is that they have a wrinkle: A bit like slot machine algorithms, IPOs tend to produce an attention-grabbing early payoff, but over the longer run, they’ve been a loser’s game.

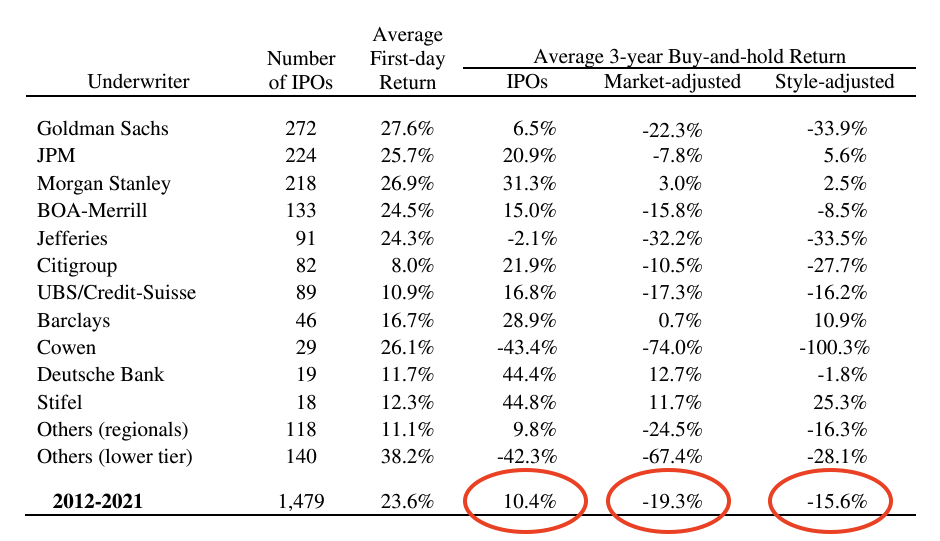

I’ve seen various data points over the years showing this, but here’s a recent set I grabbed from Jay Ritter, an IPO expert at the University of Florida.

It shows IPO performance from 2012 through 2021 – nearly 1,500 IPOs in total.

The average first-day return was close to 24% – the great, attention-grabbing piece that makes you think that IPOs are something you want to get in on, too. (IPOs tend to be deliberately underpriced for a variety of reasons, some obvious and some debatable.)

But then there’s the hangover: Although those IPOs had, on average, risen by 10.4% in the three years post-IPO, the rest of the market had risen by 19.3% more. (Even adjusting for “style” of stock left 15.6% underperformance.)

Now, logically, an IPO is one of the major paths a company takes to becoming publicly traded on an exchange. We cannot hate every company that’s had an IPO, because we might end up hating most public companies.

The point is to be careful investing in IPOs because they’re IPOs.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.