Weekly Roundup: Fed Rate Cut, Trump Returns, Bad Buffett ETF, Next Decade of Stock Returns

Trump to return as US President

Obviously it’s the biggest news of the week, even for investors, so I’m mentioning it to let you know why I’m not mentioning it – I’ve got an entire BBAE Blog article out about it, so please see the full article for things Trump.

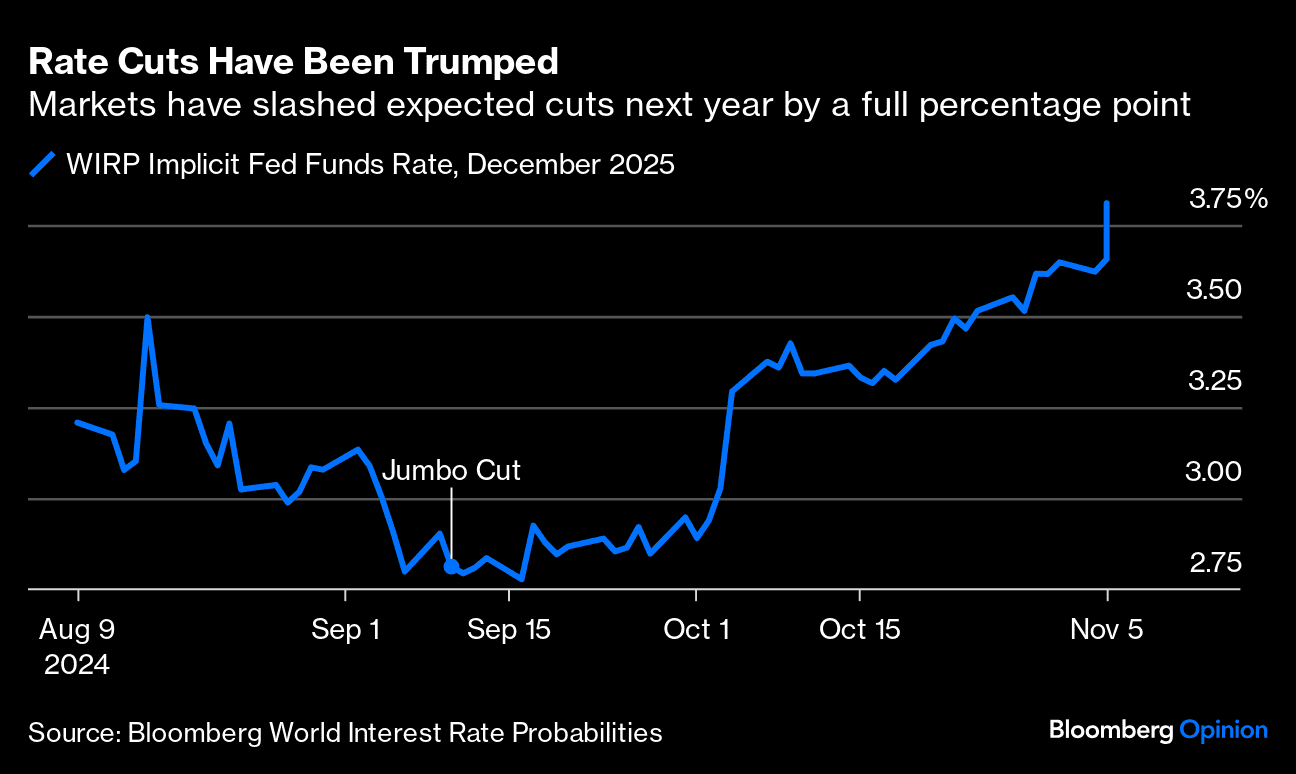

Fed rate cut

With everyone talking about Trump’s win, it’s easy to forget that the big news of the week might otherwise be the Federal Reserve’s quarter-point interest rate cut.

Maybe it’s non-news news, in the sense that everyone was expecting it. It’s good for small caps, which have much more debt than large caps (and a much higher proportion of floating-rate debt; they got clobbered by high rates, so rate drops should help undo the carnage).

It’s in principle good for weakening the US dollar, as lower-paying bonds – which, in theory, trickle up from lower Fed Funds rates, though this theory is debated by some – mean less demand for dollars to buy US bonds.

It’s also good for emerging markets, which de facto must borrow and repay borrowings in US dollars (because “nobody” trusts their currencies). And it’s good for stocks because lower discount rates increase the present values of future cash flows.

But we can’t look at this cut in isolation, even though Fed Chair Jerome Powell says the Fed is not taking anticipated Trump policies into consideration at this point. (And Jerome says he would not leave the Fed if Trump asked him to.)

Key point: If Trump does create the inflation the market expects him to – from increased government spending, from cutting taxes, from increased tariffs, and potentially from removing some amount of low-paid immigrant labor from the labor pool – Jerome Powell’s job gets harder, in the sense that the inflation he’s worked so hard to tame may return.

Translation: Expect fewer rate cuts going forward; the chance of “higher for longer” is itself higher (and probably for longer).

Worst ETF idea ever, or one of them

One perspective: In a sign the ETF market is reaching new lows, we now have this: the Kick BRK 2X Daily Long Target ETF (NYSE: $BRKX).

The purpose of this ETF is to provide 200% of the daily returns of Berkshire Hathaway (NYSE: $BRK.B).

Anyone who has any idea why a reasonable person would want this ETF, please raise a hand.

Before you say: “It’s just for fun, man” consider this: Warren Buffett and his former longtime partner Charlie Munger – perhaps the two most respected individuals in the investment world during their tenure – have designed Berkshire as an investment vehicle for really, really long-term investors.

Go to an annual meeting in Omaha, as I’ve been doing for years, and you’ll not only meet people who’ve held Berkshire for 30+ years and with no intention of selling – this guy I talked to is literally never selling – but you’ll see that pretty much the whole ethos of Berkshire is long-term-ism.

Berkshire is also a diversified conglomerate, whose daily moves are going to be muffled by virtue of having so many pieces zig this way and that. (That said, the S&P 500 is also diversified, and that doesn’t stop leveraged ETFs from springboarding off of it.)

I guess that’s my point: What’s the logic of gambling – let’s call it what it is – on the daily returns of an investment conglomerate whose internal managers and external investors alike pay no heed to short-term movements?

I’m not endorsing leveraged daily ETFs, but something like an Nvidia leveraged ETF would at least make sense for gamblers: The stock is volatile, and it’s also heavily driven by a momentum or group psychology element. Berkshire is neither of these.

Not only is it a leveraged ETF, which I’m not wild about, but it’s a leveraged ETF whose underlying investment doesn’t fit the profile. Plus, it feels almost like a sacrilege to do this to Berkshire in particular.

Another perspective: As I wrote about in the BBAE Blog several months ago, though leveraged ETFs are said to be for day traders only (95% of day traders lose money according to one study, in case you’re getting ideas), if you buy and hold a leveraged ETF that goes up over the long run, you can enjoy extremely high returns.

Now, the returns are very path-dependent and experience gut-wrenching volatility (read: drops. Nobody holding a stock ever complained about a sudden spike upward) many times along the way.

(Again, buying and holding is a hypothetical, off-label use of daily leveraged ETFs. If their underlying investments go down or even stay flat, you can lose your shirt.)

Ergo, if you’re truly a long-term, never, ever, sell type and you truly believe in Berkshire for the long run, you may be a perfect candidate for a daily 2x Berkshire ETF!

I’m joking, and nothing I say is investment advice. My point is that ironically, the best returns for daily leveraged ETFs come from buying and holding them off label, and there’s perhaps no more willing group of investors to buy and hold through thick and through thin than Berkshire investors.

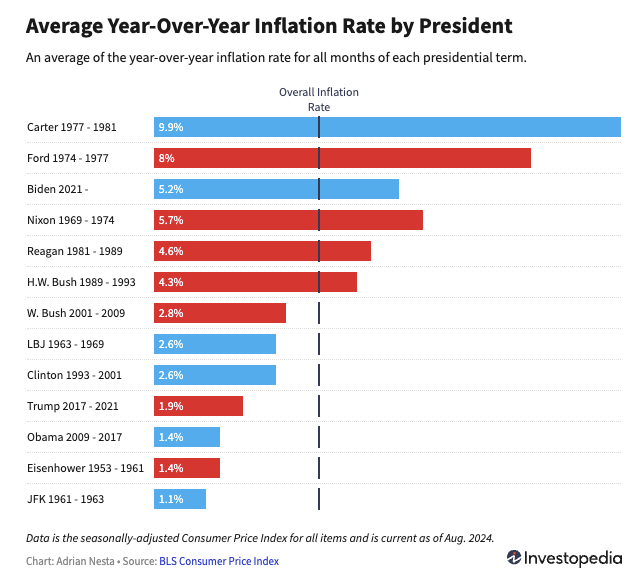

Presidents don’t control markets

Although I like Investopedia, I really don’t like articles like this. It’s very easy to overlay economic conditions on top of whoever is in the White House. It’s certainly possible for a US president to implement policies that move an economy: Reducing taxes and increasing government spending, for example, are likely to stimulate the economy.

But what about borrowing lots of money? Assuming that money is spent, it presumably stimulates the economy in the near term, too. But intuitively, it does create an obligation that “somebody down the road” will have to take care of.

There’s a time lag to many economic decisions, too. For example, Javier Mieli, PhD economist and current President of Argentina, is big on “taking the pain” now with austerity plans to massively reduce government waste – something like 35%-40% of Argentenians have been employed by the government, which doesn’t feel sustainable – and rebuild sovereign credibility after years of can kicking. Milei’s actions have sent Argentina into recession and increased poverty – as he promised – but most Argentines voted for him because they know he’s not actually causing the economic pain: The “pain” has been in the economy for decades, in the form of potential energy. Milei’s plan, if it works, aims to get the pain out of the system so Argentina can credibly rebuild.

So with those disclaimers, here’s inflation by US president, per Investopedia:

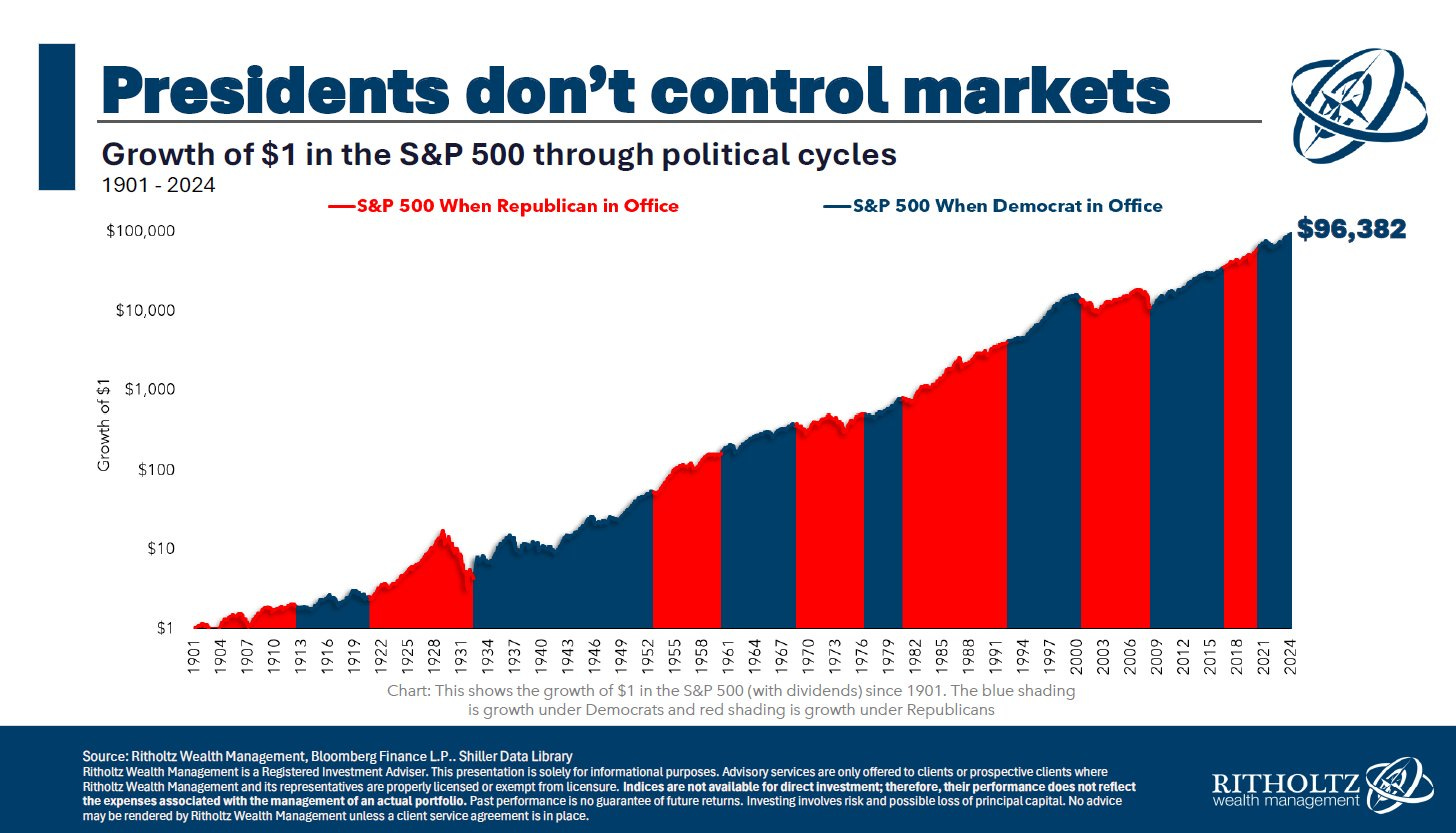

And in a graphic from Barry Ritholtz’s firm that Sam Ro of Tker.co showed in his newsletter, if you’ve been a long-term investor, who’s president hasn’t historically made a big difference. To me, this is a good thing.

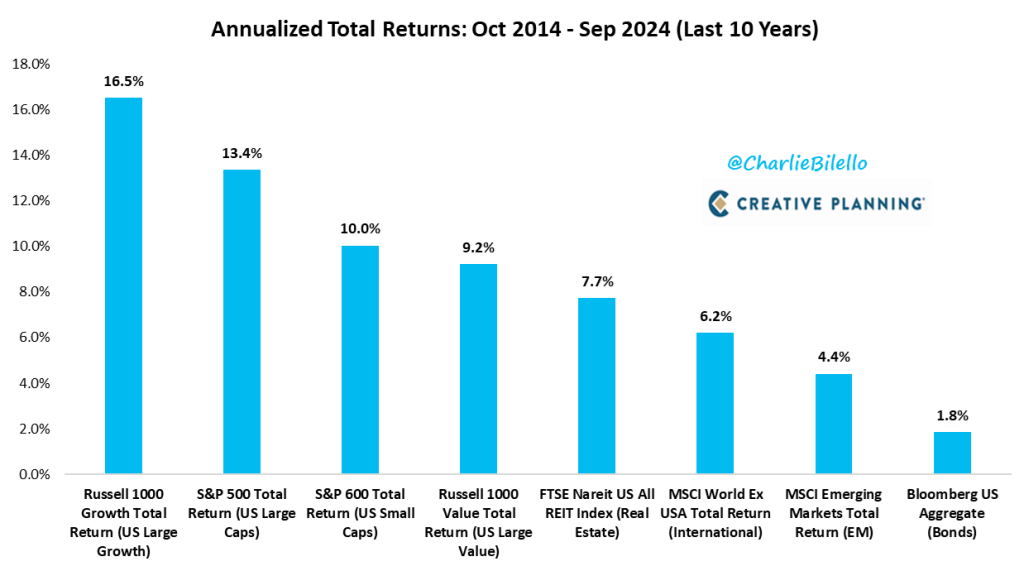

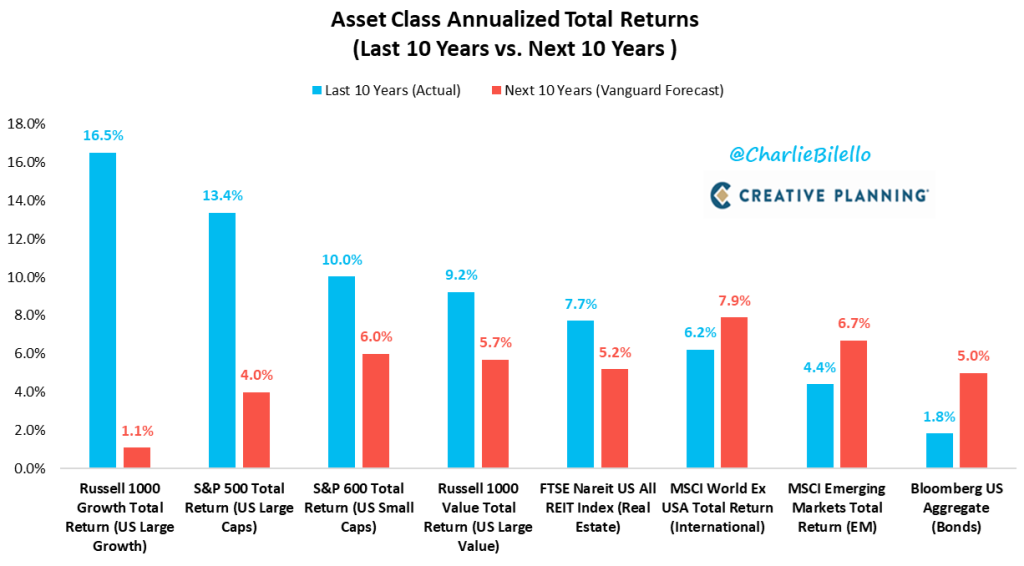

It was a US large cap (growth) decade

We knew it was, but now we can see it was. Charlie Bilello of Creative Planning has shown just how well American large-cap growth stocks did over the past 10 years – and just how poorly emerging markets did (roughly ¼ the return of US large-cap growth stocks). We knew these things, but this chart really shows some perspective.

If the US dollar stays expensive, I’d expect emerging markets to continue to underperform. Small caps should rebound, traditionally speaking, with falling rates. As for value? I can’t imagine it never coming back, but given that people have been incorrectly calling for value’s return for more than a decade (same for emerging markets’, incidentally), I’m not making any predictions.

Vanguard is, though – and they’re predicting almost an inverse of what’s been hot in the past 10 years, bonds excluded.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.