Weekly Roundup: Nvidia, Apple, and Microsoft Lead, Regional Banks, Investing Pays Off

US Markets in a Large-Cap Semiconductor Mood

I’m not complaining, but markets keep defying some of the traditional laws of physics. At least that’s one perspective.

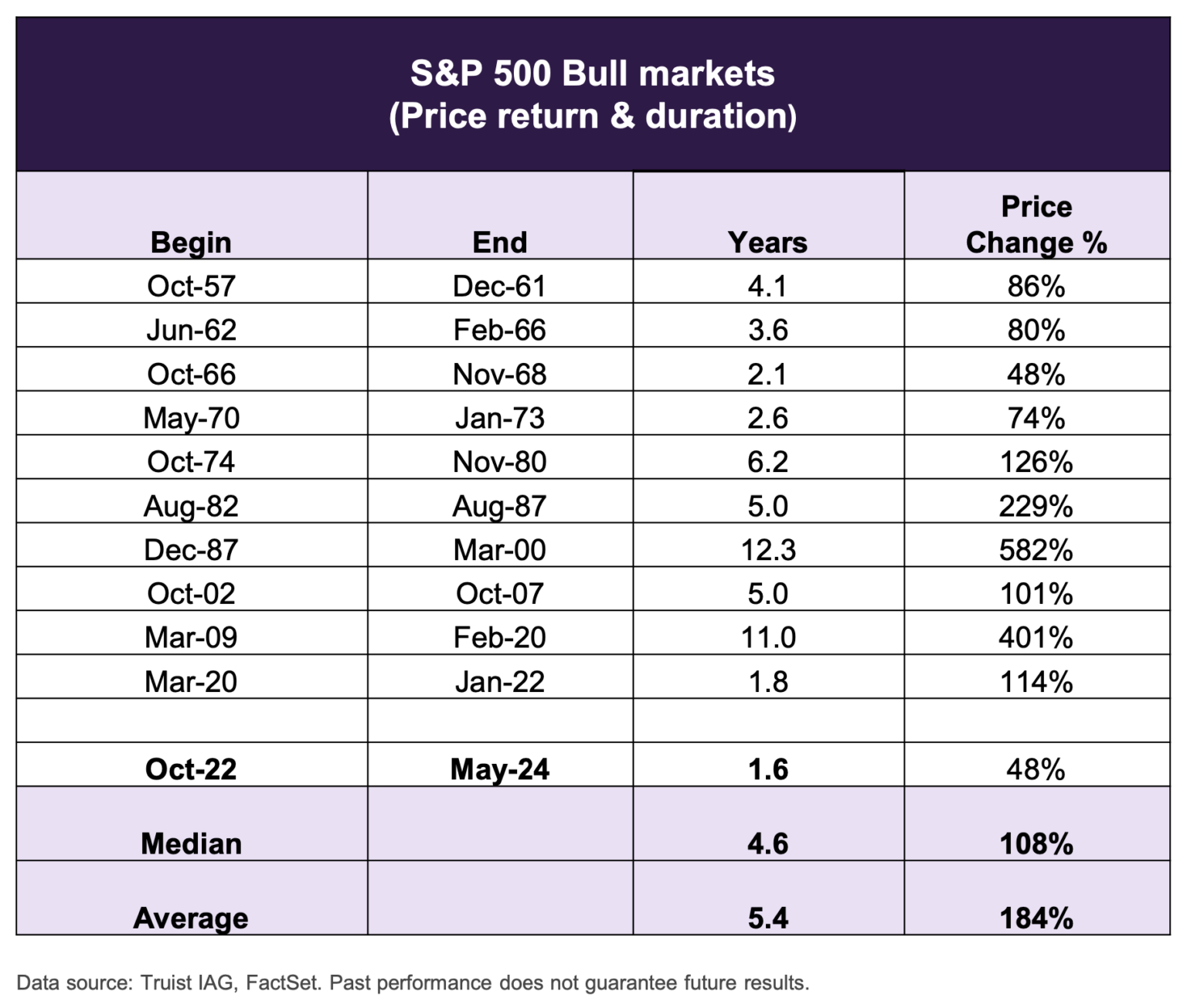

But first, good news from Sam Ro of Tker.co, who cites a chart from Truist showing that actually, the current bull market is still below average in terms of length and price change.

I tend to think valuation is a more relevant factor in measuring the “bull-ness” of bull markets than just time and price change, but time and price change are something, and it’s interesting to know that things aren’t terribly off the hook by those measures.

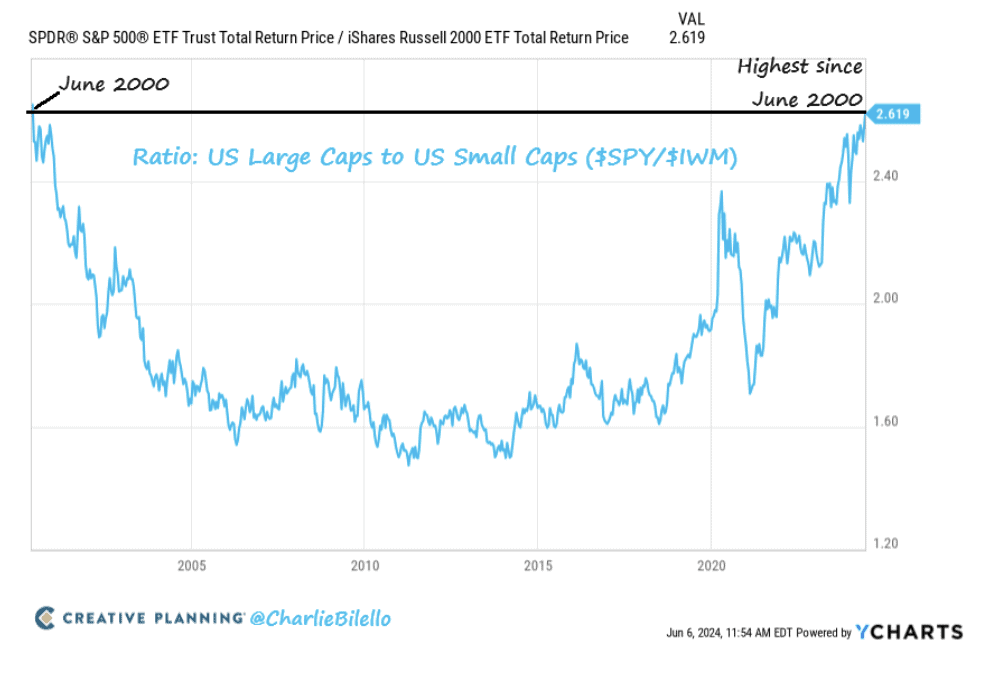

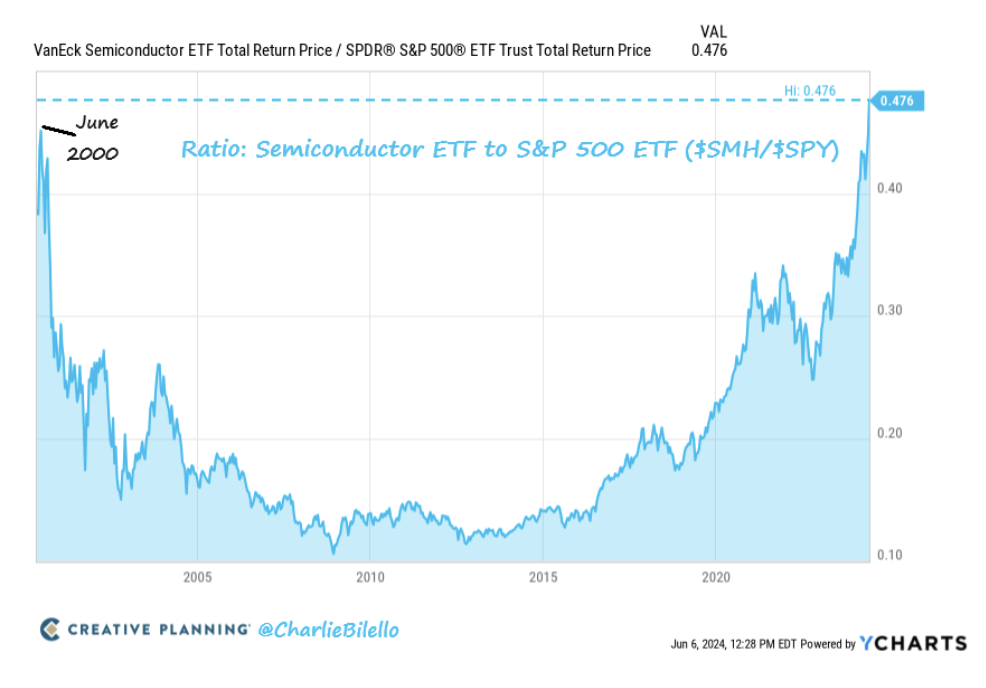

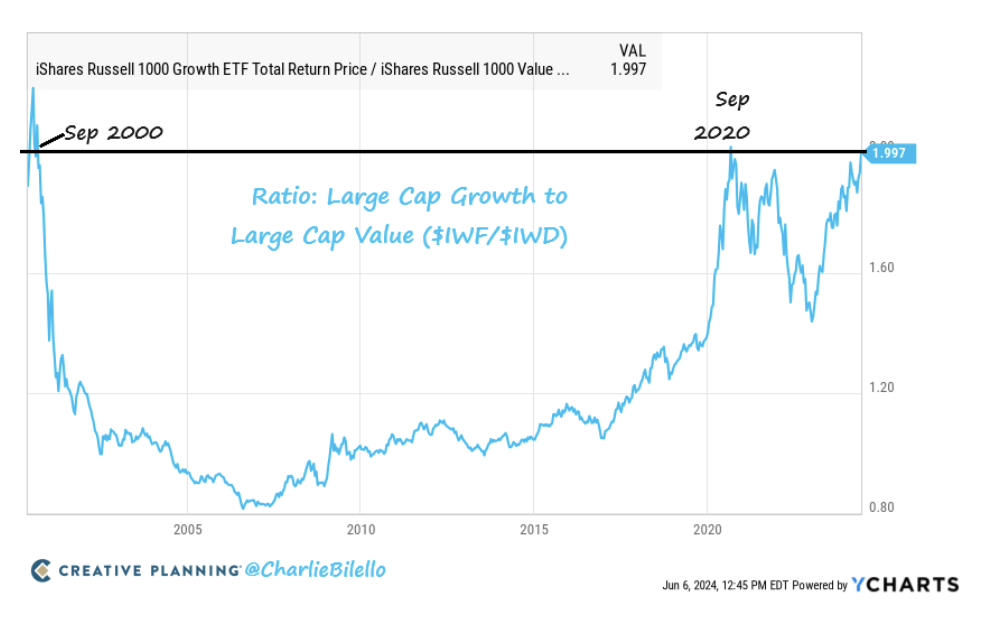

Enter Charlie Bilello of Creative Planning. I’ll show a few graphs from Charlie’s excellent newsletter this week because I feel they’re, well, excellent at making their points.

You may recall my PE and Shiller PE charts from last week’s commentary showing that stocks have been getting more expensive on a PE ratio basis.

As you might guess, those valuation gains are very large-cap dominated. And they have not been more large-cap-dominated in nearly a quarter-century.

And if you follow the news, you know it’s not just any large caps that are dominating. It’s techy large caps, and especially semiconductor large caps.

And, not surprisingly, it’s a growth-focused large-cap market, versus a value-focused one. (As a side note, this is why we chose MarketGrader to power BBAE’s smart beta portfolios – MarketGrader’s algorithm doesn’t particularly favor either value or growth, making it akin to an all-terrain vehicle for markets.)

MarketGrader founder Carlos Diez and I both dislike the “growth vs value” dichotomy for being overly simplistic – any time you buy a stock, you’re implicitly declaring it undervalued – but generally, growth stocks have higher sales growth, higher valuations, and more exciting-looking futures, whereas value stocks are the boring, unloved, nobodies of the market that have the benefit of low investor expectations.

So, no surprise in a sense, with Nvidia (Nasdaq: $NVDA) briefly joining the $3 trillion club and Nvidia, Microsoft, and Apple making up 20% of the S&P 500 by market cap.

I can’t predict the future, but I can tell you that generally, investors have made the biggest money betting on surprises, versus the expected thing.

What could that surprise be? Well, AI could either be bigger or smaller than the market expects. I just wish I could tell you which. My guess, based on how things have worked in the past, might be smaller for the near term, and perhaps larger ultimately – and good returns in new industries tend to come with a lot of collateral damage. That said, I’d be afraid to bet against Nvidia.

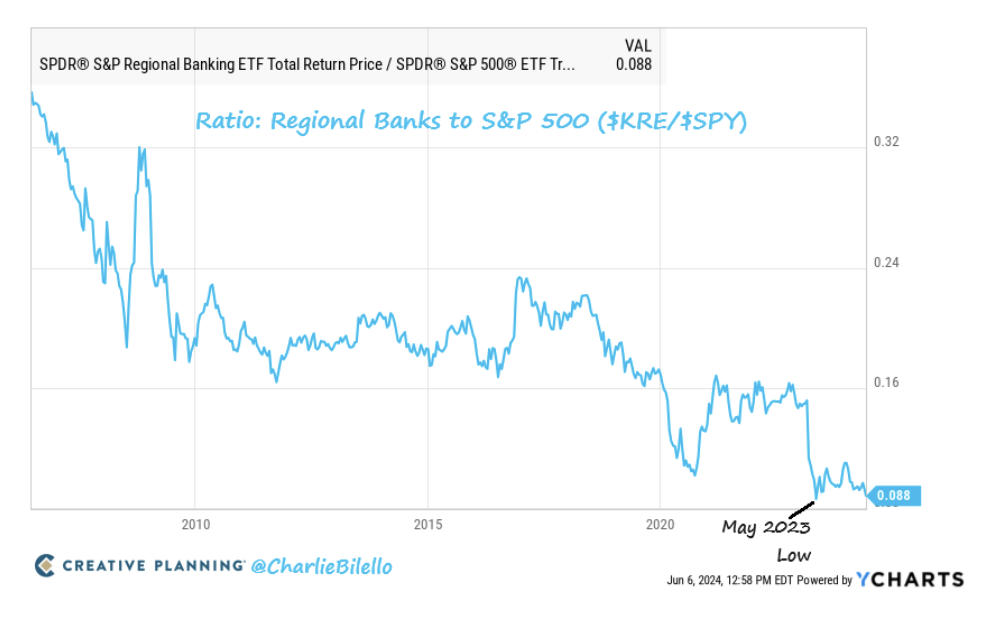

Great values in regional bank stocks?

Speaking of value and speaking of Charlie Bilello, he shows just how far one regional bank ETF has fallen relative to the S&P 500 (technically, relative to an S&P 500 ETF).

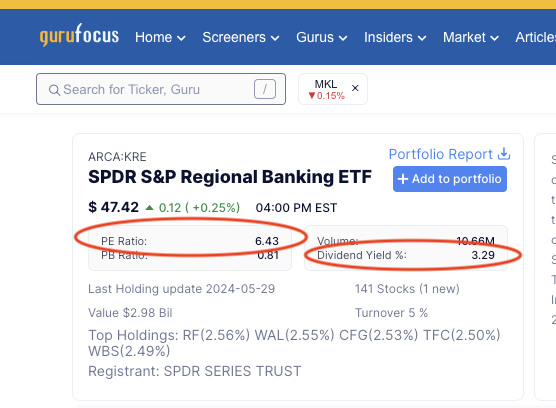

Whereas the S&P 500 trades at a PE of nearly 28 per Multpl.com, the SPDR S&P Regional Bank ETF (NYSE: $KRE) trades at a PE of… wait for it… 6.43. This is with a 3.29% dividend yield, too.

As with AI on the upside, I think it’s easy for investors to have the wrong discussion here.

On one hand, whatever the bad news is causing the price drop, unless regional banks are going to zero, there is absolutely a point at which, bad news and all, regional bank stocks are a wonderful buy. (Invert this for AI: World-changing as it may be, there is a valuation point at which stocks start to incorporate far more good news than could ever really happen.)

On the other hand, the regional banks’ bad news seems as bad as the AI stocks’ good news is good: Post-COVID, commercial real estate is getting killed, and real estate tends to be a local game, and thus real estate loans tend to be made by local and regional banks.

Even though companies went hybrid or even all-virtual during and after the pandemic, office leases tend to be surprisingly long-term (office leases may be anywhere from 5 years to 15 years, with 5-10 years probably being the most common), and lessees – companies – have been financially strong, and thus able to pay their leases, regardless of how much they were actually using the space.

But, finally, as New York Community Bank showed us earlier in the year, the ugly reality of lease renewals is hitting the market, and under-construction office buildings that have finally been completed are struggling to find tenants.

A New York office building sold for $1 a few months ago. A Washington, DC office building once assessed at $72 million has sold for $16 million. And an empty San Francisco office building once priced at $62 million has sold for $6.5 million (registration required, but you can still see the headline, which is basically the whole story).

I’m sure there are many more versions of this story, especially on a smaller, less-newsworthy scale, all across the US. Who eats these price declines? Initially the building owners. But in many, and perhaps most, cases, the building owners own the building thanks to loans from regional banks.

And then there are the marks.

Even if you’re not planning on selling your near-vacant office building, or rental building, or whatever building, the fact that many buildings around yours are selling for fire-sale prices means you have to “mark” down the value of your building. You’ll pay lower property taxes, but a big markdown may trigger collateral covenants in your loan contracts, requiring you to pony up cash or assets that you may not have.

Perhaps you decide it’s best to just be the next guy to sell your near-vacant building at a fire-sale price.

I wish I could tell you the exact breaking point of the AI hype – the moment investors’ switch should flip from “run to” mode to “run away from” model. Likewise, I wish I could tell you when the commercial real estate-driven regional banking despair has run its valuation course and the stocks have now become fantastic buys. My guess is that we still have a fair bit more real estate repricing ahead of us, given the long-term nature of the contracts.

I can’t tell you when. But I can tell you that that’s the way you could be looking at these things. It’s too superficial to say: “AI will be big! I’m going to buy AI stocks!” It’s also too superficial to say: “Regional banks have been pounded way down – so I’m going to buy!”

Of course, you (generic “you,” vs. you personally) could get lucky. And those who get lucky tend to never attribute anything to luck. (Said by someone who’s absolutely attributed luck to skill before.) But the reality is that good investment decisions are never one-dimensional. There’s always a weighing involved – or should be.

Americans’ Investments are Paying Off

Good news, mostly: Americans scored more dividend and interest income than ever before – a seasonally adjusted $3.7 trillion in the first quarter. That’s $770 billion higher than four years ago, per this Wall Street Journal article (subscription or registration may be required).

Higher interest rates and an ebullient stock market riding AI hype may be behind this good news, but as is often the case in economics and markets – or at least when anticipating Federal Reserve moves – good news can be bad news, and vice versa. All this investment income will presumably lead to higher spending, which will presumably keep inflation from falling as much as the Fed wants, which will presumably delay the Fed from lowering interest rates to stimulate the economy (or at least restrict the economy less, if you prefer that view).

Why stimulate an already-stimulated economy? That’s exactly what the Fed is asking.

The success of US market investors in this higher interest rate (and high stock market) climate brings two points to mind:

- Move over, haves and have-nots: The world will always have them, but a more actionable viewpoint is that as long as capital markets remain strong, the wealth accumulation divide in developed countries will be between those who participate in compounding and those who don’t. Compounders, and compounders-not, in other words. And if you’re reading this, I’m pretty sure that you’re an investor – and thus a compounder. Good for you!

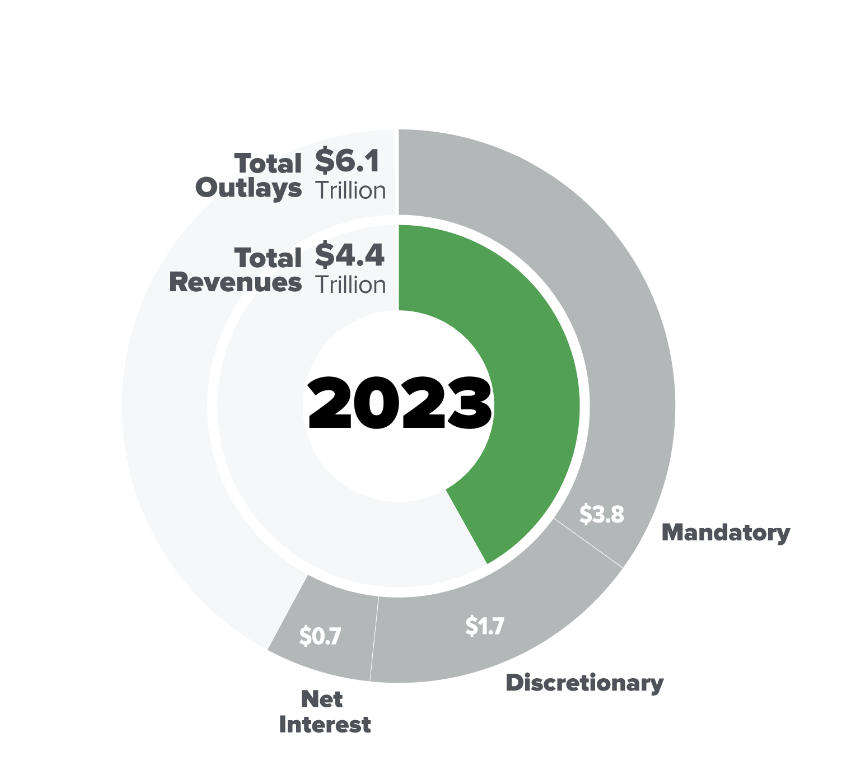

- Higher interest rates may be good for US investors, but they are not good for the US government. Uncle Sam famously (semi-famously) did not refinance much debt when rates were super low a few years back – that and when you take in $4.4 trillion in taxes yet spend $6.1 trillion, that leaves $1.5 trillion to come from… somewhere?

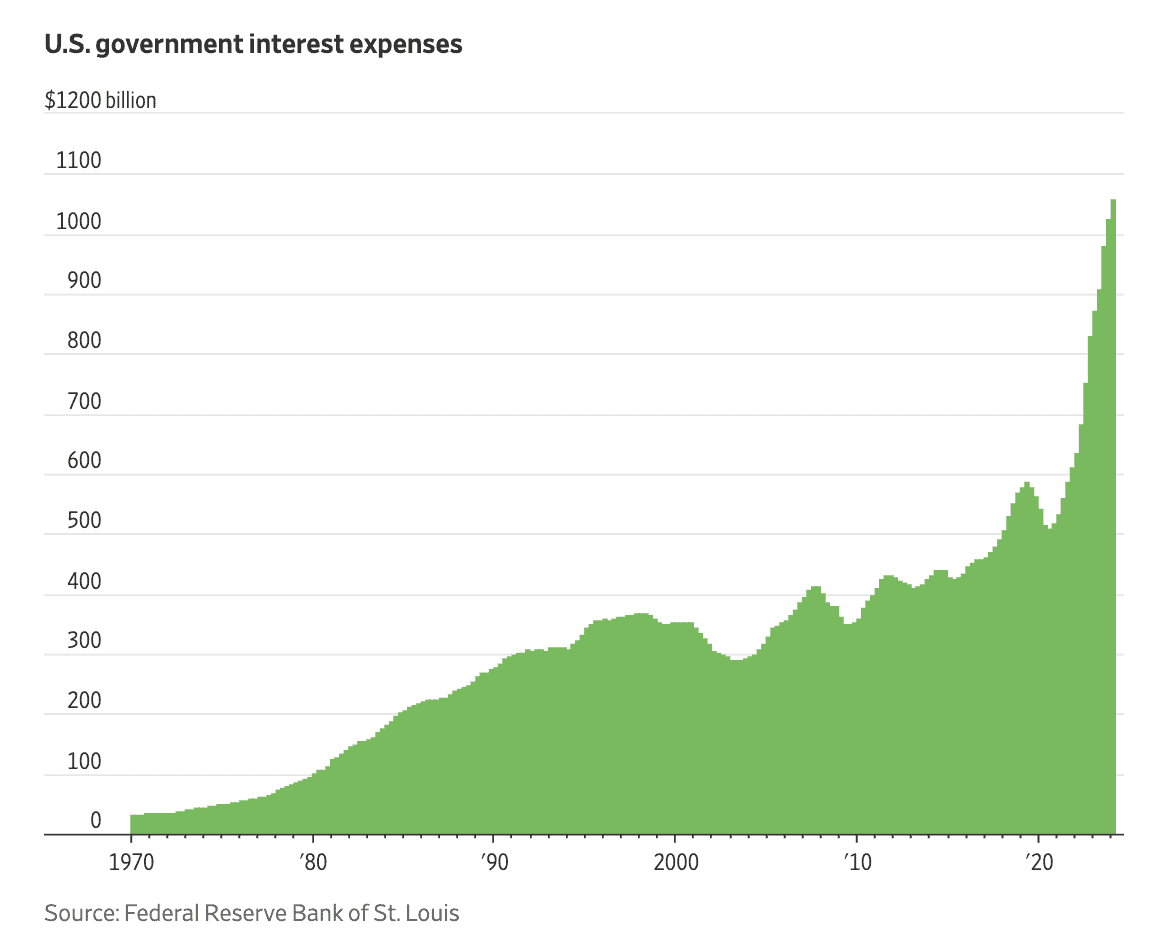

That “somewhere” is debt. And not only is America’s debt growing, per the Wall Street Journal graphic below, the interest expenses on that debt are growing too, which makes logical sense.

How does this party end? In the past, such as during and after the debt the US accumulated to fund World War II, the US simply outgrew its debt, to paraphrase Morgan Housel. In fact, that’s what has essentially always happened. But as with AI hype and regional bank despair, all things in economics have at least theoretical limits.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. James owns shares of Apple. BBAE has no position in any investment mentioned.