What Does Warren Buffett See in Ulta Beauty ($ULTA)?

Buffett Buys Ulta Beauty.

We saw plenty of headlines last week about this.

Even if you’re new to investing, you’ve probably noticed that any time Warren Buffett (or, really, Berkshire Hathaway (NYSE: $BRKB) his investment company) buys or sells a stock, the media gets buzzing.

I’ve already covered why Buffett is a great investor (and your trusty BBAE team is on the ground at Berkshire Hathaway’s annual meeting in Omaha every year).

For this piece, let’s go behind the news articles and dig deeper into Berkshire’s recent Ulta Beauty (Nasdaq: $ULTA) purchase. If you’re new to investing, you’ll learn some basic fundamental analysis, and seasoned and new investors alike will get a new idea to explore.

The closest Ulta to BBAE CIO James Early.

First, Buffett probably didn’t buy Ulta Beauty.

“Buffett Buys Ulta Beauty” is a catchier headline than “One of Buffett’s Lieutenants – Either Todd Combs or Ted Weschler – Likely Bought Ulta Beauty on Behalf of Berkshire Hathaway,” but in reality, that’s almost certainly what happened.

Buffett has noted how hands-off he is with Todd and Ted, and that he tends to find out what they’ve been up to when (or just before) everyone else does – when Berkshire is reporting its SEC filings.

Note that while Berkshire’s $266 million Ulta purchase sounds big to you and me, for Berkshire, it’s just 0.08% of Berkshire’s $314 billion in equity holdings, and just 0.14% of Berkshire’s $190 billion in cash. In other words, it’s rounding error for Berkshire, and even Ulta’s entire $18 billion market cap would be less than 10% of Berkshire’s cash.

Still, Ulta shares rose 15% on the news.

What’s Ulta Beauty’s Angle?

Ulta Beauty started a low-pressure way to sell cosmetics, one which was later copied by LVMH’s Sephora.

Years ago, you (if you were a cosmetics buyer) had two places to buy cosmetics: the drug store and the department store. And maybe the salon, too.

Drug store cosmetics weren’t high end, and while the free, time-consuming makeover the department store gave you was nice, it was a lot of fuss, the makeup artist usually worked for one specific brand, and the process was structured to tug on your strings of reciprocity: It’s hard not to buy something from a fellow human who just spent 30 minutes working on you and is now staring at you expectantly.

Nice not to be swarmed with salespeople, although being a male may have influenced that.

Enter Ulta Beauty: Founded in 1990, it began as a discount retailer of everyday cosmetics – with self-serve free samples – but quickly climbed up the value chain to offer high-end cosmetics in a lower-pressure shopping environment (these days, Ulta is roughly 40% mass market and 60% high-end). Salespeople are available when you need help, but they’re not smothering. And Ulta grew to add in-store salons, too.

Ulta has roughly 34% of the US specialty beauty market, and offers major-brand items as well as its own private label products (which are just 3% of revenue). Makeup is modestly less than half of Ulta’s revenue; haircare and skin care are roughly 20% each, and fragrances, bath, and body items make up the rest.

Why Buffett’s helpers like Ulta Beauty

As a fundamental investor myself (and a former deep-dive hedge fund analyst, as well as leader of an equity research department), I can say that Ulta presents a nice cocktail of a well-run business with a largely sustainable advantage, a high ROIC, strong financials, good management, an affordable price, and a recent downward catalyst that may not be as bad as the market thinks.

In other words, it’s a Buffett-y kind of stock.

Ulta has strong financials

Ulta’s financials are squeaky clean, and the company sports both monster ROE (which is to be expected for a company that buys back as many of its shares as Ulta does – roughly 20% of outstanding shares have been repurchased and retired – and monster (i.e, 25%+) ROIC, or return on invested capital. I’ve talked about ROIC before and consider it the single best metric for evaluating a business’ health. I won’t rehash ROIC here, but roughly speaking, even a 12% ROIC would be good for most companies, and Ulta does more than double that – consistently (no registration required, but be prepared for aggressive pop-ups).

Operating margin is arguably the most important margin, or at least the one that tells you the most about the business, and Ulta’s is 14.7%. For comparison, Forrester Research says the average retail operating margin is 4.5% to 5%, so Ulta’s is almost thrice that. It wasn’t always this high, but crept up slowly over the years, which evidences both good management and a good business model (as well as the fact that Ulta has “earned” the right to carry higher-end (and higher margin) brands over the years as top-tier cosmetics companies felt safer with brand affiliation).

Ulta has loyal, spendy customers

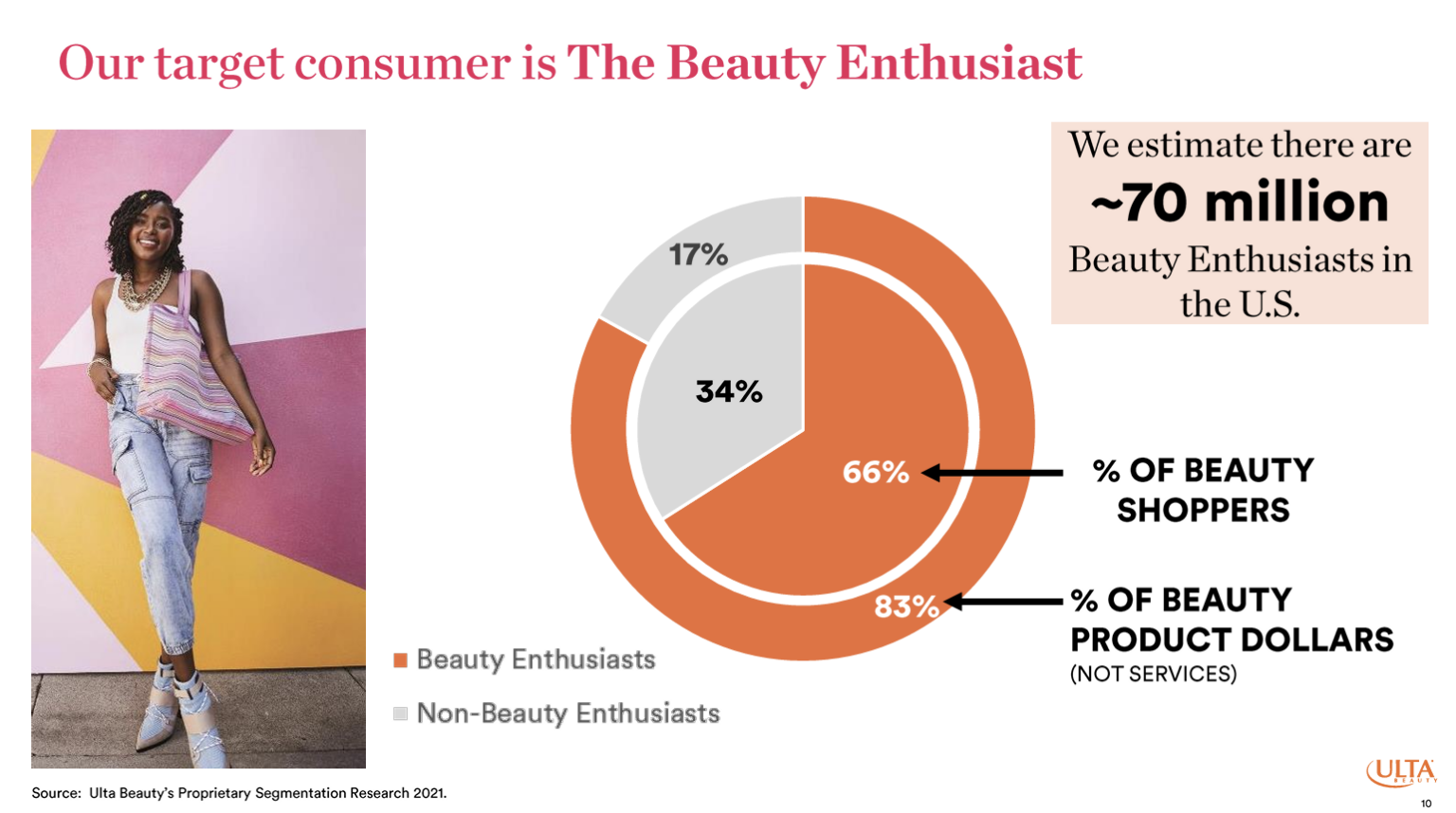

More than 95% of Ulta’s sales come from Ultimate Rewards members (roughly 45 million members, or one in every 13.5 Americans or, roughly, one in every 27 females – and if we remove females too young or too old to use cosmetics, as well as those who just aren’t the makeup type, an amazingly large portion of US makeup users are Ulta Ultimate Rewards members).

Ulta says 70 million hardcore “beauty enthusiasts” (their target market) in the US – representing 66% of beauty shoppers but 84% of beauty spending. These Ultimate Rewards customers spend an average of $200 per year at Ulta; I don’t know how that compares to other similar retailers, but it feels high to me.

And although salon spending proper is just 3% of sales – that may go higher after the company’s efforts to poach top stylists bears fruit – salon customers are cash cows: They visit Ulta twice as often and spend three times as much as regular customers.

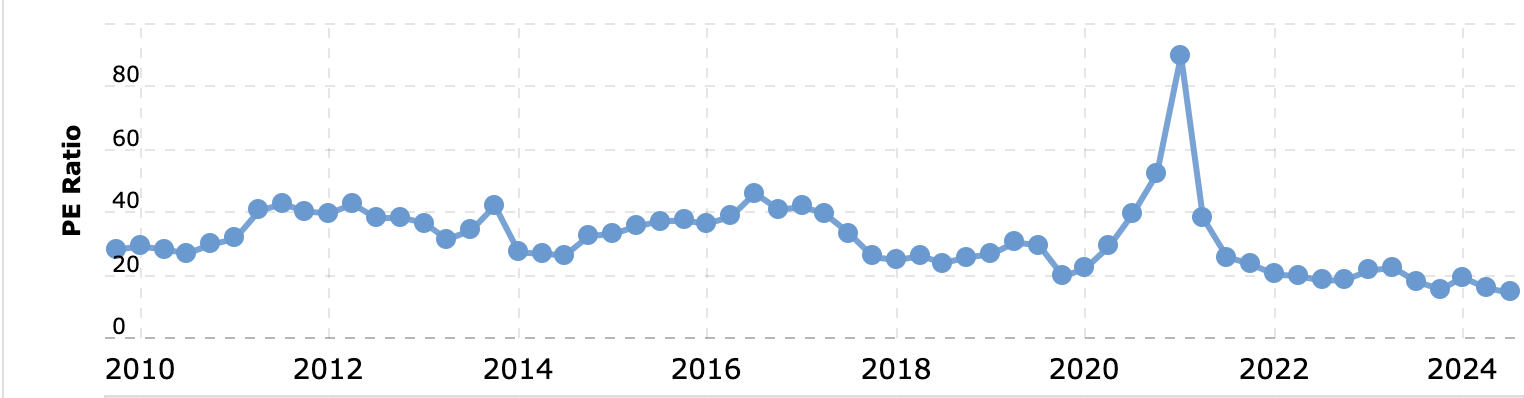

Ulta trades at a low valuation

Another thing that surely caught Todd’s or Ted’s eye was that Ulta trades at a P/E ratio lower than most retailers, and lower than the company’s long-term average.

The point I’ll add about this is that buying a stock that’s getting cheaper and cheaper only makes sense if you see a reason for it to not keep getting cheaper at some point in the reasonably near future.

What’s the catalyst for Ulta’s P/E to go back up? That’s a key question.

Ulta is slowing, but still has room to grow

Trees don’t grow to the sky, and the 10%+ annual sales growth Ulta enjoyed in prior decades will look more like 5% in future years according to analysts. That’s still double the long-term 2.5% or so the US economy tends to grow at – but it’s slower than what Ulta investors have gotten used to.

Ulta has no international stores at present, and has 1,421 stores in the US (relative to 1,638 Sephora stores in the US, though Ulta’s stores are roughly twice as large and Ulta is the market leader by sales). Ulta thinks it can get to 1,700 US stores and then focus on Canada and Mexico expansion.

Ulta has sound management

CEO Dave Kimbell, Ulta’s former president, replaced Mary Dillon, who’d been CEO since 2013, in 2021. Nothing against Dave, and he seems solid, but I really liked Mary.

A company-lore anecdote is that six months into Mary’s CEO term, while on a family ski trip in Utah, she donned a black Ulta employee uniform and pitched in to help at the nearest Ulta store on Christmas Eve.

After being surprised by how many coupons Ulta customers used, she decided that being a brand affiliated with bargains dragged down Ulta’s image. She had the company shift from coupons to free gifts instead, and she went all-in promoting high-end brands like MAC and Lancome. It worked, as the margins attest.

Why Ulta’s Stock Price Has Yo-Yo-ed

Since its 2007 IPO, Ulta has done a fantastic job of outperforming the S&P 500 – it’s up more than 5,600% versus just 600% for the S&P 500.

Ulta’s stock is down this year on poor 2024 guidance, fears of competition, and disappointing same-store sales (1.6% growth reported in the first quarter of 2024 versus 3.5% expected). Ulta stock, in fact, was down 42% this year before Berkshire bought. But as The Wall Street Journal points out (subscription or registration may be required), EPS estimates for this year are only down 5%. That’s a mismatch that Todd or Ted likely sees as a market overreaction.

A negative: more competition is coming

The big reason Ulta’s price got slammed so much is competition. For the longest time, Ulta had the tailwind of department stores going belly up, and had only Sephora to contend with in terms of non-department store, non-salon sales of high-end cosmetics.

Now, smaller Sephora is expanding into 1,000 Kohl’s, which likely means it will take market share from Ulta.

Taking market share doesn’t axiomatically mean lower revenue: Many first-to-market products or store concepts – Tesla, Kleenex, ketchup, Walmart – lost market share as competitors popped up while still growing revenue simply because their category was growing. But Ulta’s investors had been used to Ulta taking market share from everyone else, so this was a change.

Indirect competition is intensifying, which is unsurprising considering that would-be competitors have been eyeing Ulta’s juicy margins.

Walmart has a new L’Oreal deal, and Amazon has been amping up its Amazon Premium Beauty with a Clinique deal.

Cosmetics may be one area where in-person sampling is still a boon, but 20% of Ulta’s own sales are online now, and if Amazon is eyeing your category, even obliquely, it’s got to cause some worry. Luckily, Ulta, as the nation’s largest beauty retailer, has been able to keep its prices at or below Amazon’s.

The bottom line on why Ulta Beauty is a Buffett-y investment

Warren Buffett started as a value investor in the 1940s and 1950s. “Value” is sometimes (mis)equated with plain fundamental investing these days, but originally, it actually meant buying “bad” companies that often scored poorly on the sorts of attributes I covered in this article. At a cheap enough price, even a bad company can become a good investment.

Buffett’s fund eventually outgrew value investing (as copycat competition crowded in), and partner Charlie Munger persuaded him to find really good companies instead, and not be afraid to pay up for them.

It worked for Berkshire – Buffett’s slight modification tends to be pouncing on a good company when it’s beaten down for what he believes are temporary reasons – and no doubt Todd and Ted are seeing in Ulta Beauty a stock that fits the modern Buffett mold.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.